Only 0.4% of B2B SaaS startups reach $10M ARR. Of those, roughly 30% reach $50M within five years. Twenty-three percent plateau permanently somewhere in between. For Sarah Chen and the founders inside the $10M-$50M ARR band, the math is brutal: you have already beaten the odds, and you are now standing at the most demanding gauntlet in the SaaS lifecycle.

The SaaS scaling playbook from $10M to $50M ARR is the architectural sequence of organisational, financial, and go-to-market transformations that move a company from founder-led execution to executive-led predictable growth. It is not a matter of doing more of what worked at $5M. It is a matter of replacing the operating system entirely. The companies that successfully traverse the band share a recognisable pattern. The companies that stall share a recognisable pattern too. This guide unpacks both.

What follows is a 2026 framework grounded in benchmarks from ICONIQ Growth, Bessemer, OpenView, McKinsey, and 800+ scaled SaaS companies. We cover the 5 scaling stages with metrics at each, what changes structurally, what must never change, the 7 stall patterns, named case studies, and the 90-day diagnostic for any CEO asking "are we tracking to $50M or stalling?"

Strategic Intent

The $10M to $50M band is where SaaS companies stall, not from product failure but from operating-system failure. Replace the system in five stages. Hire ahead of stalls. Defend the north star. Execution does the rest.

The $10M-$50M reality: why most companies stall

The plateau is rarely a product problem. Companies at $10M ARR have already validated product-market fit. The plateau is almost always a go-to-market or organisational misalignment. The Mendoza Line research from Kellblog quantifies the natural growth deceleration: best-in-class SaaS companies retain 80-85% growth persistence year over year. A company growing 100% at $10M will grow approximately 80% the following year, 64% the year after that. Companies in the band hit a median 25% annual ARR growth, with top-quartile performers achieving 40-50% and best-in-class 50-100%.

The structural cause of plateauing at $15M-$25M ARR is almost always one of three things: the founder is still selling and has hit the ceiling of founder bandwidth, the sales team is generalist when it should be segmented, or the company has overstretched into multiple ICPs without dominating one. First Round Review's PLG-to-enterprise research documents that pure product-led growth typically caps out around $15M-$25M ARR; companies that fail to layer sales-led motion at that point stall and watch competitors with hybrid motions take the upper segment of the market.

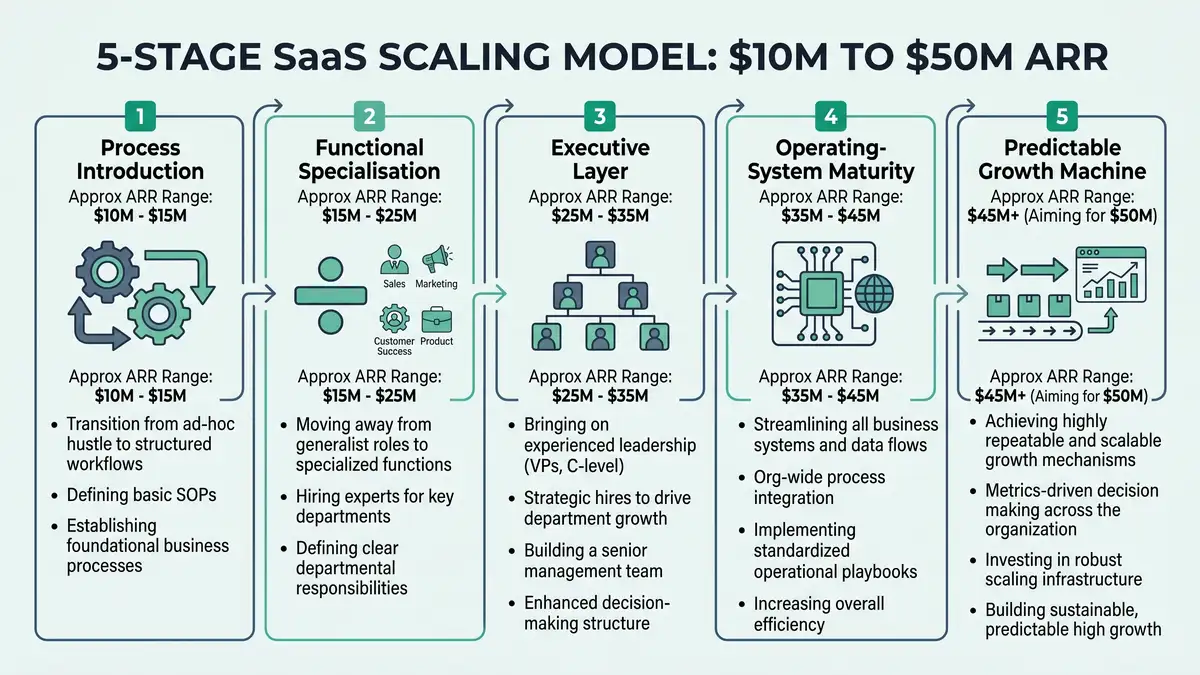

The 5 stages of scaling from $10M to $50M ARR

Scaling is not linear. It moves through five discrete stages, each defined by ARR threshold, organisational shape, KPI focus, and operating cadence. Skipping stages is the single most expensive mistake at this band.

| Stage | ARR Band | Org Shape | Key Hires | Primary KPI Focus | Rule of 40 Target |

| 1. Process Introduction | $10-15M | Founder + 1 VP | VP Sales, Head of CS | Sales motion repeatability | 40% growth / -20% margin |

| 2. Functional Specialisation | $15-25M | 3-4 VPs | CMO, VP Engineering, expansion ops | Segmented GTM motion | 35% growth / -10% margin |

| 3. Executive Layer | $25-35M | CRO + exec team | CRO, CFO, VP People | Multi-channel scale | 30% growth / 0% margin |

| 4. Operating-System Maturity | $35-45M | COO or CRO consolidation | COO, Head of RevOps, Head of IR | Operating-system discipline | 25-30% growth / 10% margin |

| 5. Predictable Growth Machine | $45M+ | Full exec layer | Backfills + international leads | Compound growth + margin | 25% growth / 15% margin |

Source: peppereffect scaling model + ICONIQ Growth 2025 GTM + Intelligent Business Rule of 40 benchmarks.

Premature Profit Optimisation Trap

The most expensive mistake at $12M-$15M ARR is cutting growth investment to manufacture 20% EBITDA margins. McKinsey's Rule of 40 research shows companies that starve the engine at Stage 1 or 2 signal a capped TAM to acquirers and destroy $30M-$100M in future enterprise value. Run negative margin at Stage 1-2 with confidence if growth is above 35%.

What changes structurally between $10M and $50M

Eight things change. None are optional. Founders who fight any of these eight changes are the founders who stall.

Org chart: founder-led to executive-led

At $10M ARR the founder is still in every deal. By $50M, an executive team of 6-8 functional leaders runs the company; the founder works on strategy, capital, and culture. The transition typically completes by $30M ARR. Founders who do not let go by $25M become the bottleneck themselves.

Sales motion: founder-led to segmented

$10M ARR has 2-5 generalist AEs trained by the founder. $15M ARR introduces segmentation (enterprise, mid-market, SMB). $25M ARR adds SDR layer with documented qualification handoff. $35M+ adds geo or vertical specialisation. Generalist sellers at $25M ARR are the symptom of a stall.

Hiring velocity: 1-2/month to 5-10/month

$10M ARR adds 1-2 hires per month. $30M-$50M ARR adds 5-10. The hiring infrastructure (recruiting team, interview loop, onboarding playbook) must precede the velocity. Companies that scale hiring without infrastructure produce 12-18 month tenure averages that destroy compounding.

GTM channels: 1-2 to 4-6 diversified

$10M ARR typically rests on 1-2 channels (outbound + inbound, or PLG). $50M needs 4-6: outbound, inbound, partner channel, paid acquisition, community, AI ecosystem. Channel concentration above 50% at $30M+ ARR is a board-level risk.

Customer segments: SMB to mid-market to enterprise

$10M ARR often serves one segment. The $50M trajectory typically requires segment expansion (SMB-to-mid-market, or mid-market-to-enterprise). Each expansion introduces different sales cycles, ACVs, and onboarding. Trying to serve all three with one team is a stall pattern.

Pricing complexity: 1 plan to tiered to enterprise custom

$10M ARR usually has 2-3 plans. $50M needs tiered usage-based pricing, enterprise custom contracts, and a deal desk. Pricing complexity must come with pricing operations (a Pricing Manager by $25M, deal desk by $35M).

Operating cadence: weekly to instrumented

$10M ARR runs on weekly leadership meetings and ad hoc dashboards. $50M runs on an instrumented operating system: weekly business review, monthly board prep, quarterly strategy, real-time dashboards, integrated forecasting. The Cadence (David Sacks) is the canonical reference.

Capital structure: ad hoc to disciplined

$10M ARR finance is the founder plus a controller. By $50M ARR, a CFO leads a finance team, manages a 13-week cash forecast, runs board reporting, and prepares for the next round or exit optionality. The transition typically requires a fractional CFO at $15M and a full-time CFO by $25M-$30M.

What does not change

Five disciplines must remain immovable across the entire band. The companies that hold these five constant while changing everything else are the companies that reach $50M and beyond.

North-star metric discipline. One metric. Everyone in the company can name it. It is reviewed weekly. Companies that rotate north-star metrics every quarter signal organisational drift and produce strategy that nobody follows. At Sarah Chen's stage, the north star is typically net new ARR or net revenue retention.

ICP focus. The temptation at $20M ARR to chase a non-ICP enterprise logo is real and almost always destructive. Customers outside ICP have lower NRR, higher support cost, and lower expansion velocity. Defending ICP at every stage compounds healthier unit economics for the next five years.

Founder-led culture-setting. The founder steps back from execution but never from culture. The values, the operating rhythm, the bar for hiring, the way disagreement is handled: these remain founder-set throughout the band. Founders who fully delegate culture lose the company's edge by $35M ARR.

Weekly business review cadence. One meeting, same time, same metrics, every week. David Sacks's Cadence framework documents that companies maintaining strict WBR discipline scale 30-40% faster than peers who let the rhythm slip.

Customer obsession. Customer interviews never stop. CEO joins 5-10 customer calls per month at every stage. Companies that stop hearing customer voice directly at $25M ARR produce roadmaps that diverge from market reality inside 12 months.

Want to see your own CAC against peer benchmarks? Run the CAC Diagnostic for your true CAC, the 30 to 50% reduction agentic deployment delivers, and a board-ready PDF in 60 seconds.

Run the CAC DiagnosticThe financial benchmarks: Rule of 40, Magic Number, NRR, Burn Multiple

The financial system at each stage looks different. Five metrics matter most, and the healthy range for each shifts as you move through the band.

| Metric | $10M Healthy | $25M Healthy | $50M Healthy |

| Gross Retention | 85-90% | 90-93% | 92-95% |

| Net Revenue Retention | 105-115% | 110-120% | 115-130% |

| Magic Number | 0.7-1.5 | 0.8-1.4 | 0.7-1.2 |

| Burn Multiple | 1.0-2.0 | 0.5-1.5 | under 1.0 |

| CAC Payback | 12-18 months | 12-15 months | 10-14 months |

| Rule of 40 | 20-30% | 30-40% | 40%+ |

Source: peppereffect benchmarks + Intelligent Business Rule of 40 + Stripe NRR + OpenView 2025 benchmarks.

NRR is the single most leveraged metric across the band. A company with 130% NRR doubles ARR every 2.5 years from the installed base alone, before any new logo acquisition. A company with 95% NRR has to acquire 20% net new customers every year just to stand still. FE International's SaaS valuation research documents that NRR above 120% commands premium exit multiples regardless of growth rate. Sarah Chen's path from $15M to $50M can run on 115%+ NRR with disciplined expansion motion alone.

The 7 most common scaling stalls

Across peppereffect's audits of 60+ SaaS companies in this band, seven stall patterns recur. Each is structural and avoidable.

| Stall Pattern | Symptom | Root Cause | Fix |

| Premature VP hiring | VP brought in before motion is repeatable | Founder hires for resume, not stage fit | Hire when 2+ reps independently hit quota |

| Over-hiring in down quarters | Headcount grows faster than ARR | Plan based on optimism, not pipeline | Tie hiring to leading indicators, not bookings forecasts |

| Founder ICP drift | Chasing logo deals off-ICP | Vanity logo > unit economics | Quarterly ICP review; sales comp aligned to ICP |

| Pricing complexity bloat | 15+ plan combinations; sales confused | One-off custom deals never consolidated | Pricing Manager + quarterly pricing reviews |

| International too early | Opening EMEA at $15M ARR | Misreading deal pipeline as market signal | International at $25M+ with dedicated GM |

| Multiple ICPs at once | Sales pitches read like three companies | Fear of TAM narrowing | Dominate one ICP to 60% market share before expanding |

| Skipping the operating cadence | Decisions in Slack DMs, not meetings | Founder distaste for "process" | WBR + monthly QBR + quarterly OKRs, non-negotiable |

Source: peppereffect $10M-$50M ARR audit pattern library, 60+ B2B SaaS engagements 2024-2026.

Named SaaS scaling case studies

Gong: $10M to $200M+ on disciplined GTM. Gong grew from $10M ARR in 2018 to over $200M by 2021 by following an unusually disciplined playbook: niche ICP (sales orgs at $5M-$500M revenue), segmented sales team by Year 2, dedicated VP of Customer Success by $15M ARR, and category creation ("revenue intelligence") layered on top once the core motion was repeatable. Magic Number stayed above 1.2 for 36 months.

Notion: $10M to $100M+ on PLG-to-enterprise transition. Notion crossed $10M ARR purely on PLG. By $25M they layered sales-assist for team plans. By $50M they had a true enterprise sales team handling 7-figure deals. The transition took 30 months and required hiring three VP Sales candidates before the third stuck. The lesson: PLG-to-enterprise is the highest-failure-rate transition in SaaS, and most companies under-invest in the sales-led layer.

Linear: deliberate pace, premium pricing. Linear chose a slow scaling pace deliberately, refusing to chase non-ICP customers. ARR grew from $10M to $50M over 4 years with premium pricing (2x Jira per seat). The trade-off: slower growth, but NRR above 130% and best-in-class burn multiple. The case demonstrates that scaling speed is not the only path to enterprise value.

Drift: category creation to scaling. Drift created the "conversational marketing" category at $5M-$10M ARR, then scaled to $50M+ in 30 months by recruiting category-aligned customers and building a sales motion around the category frame. The case shows that category clarity reduces sales cycle length and enables faster scaling at the $10M-$50M band.

Figma: PLG-to-enterprise blueprint. Figma scaled from $10M to over $400M ARR by extending PLG into enterprise via team and org plans, then a dedicated enterprise sales motion by $100M ARR. The Figma blueprint is now the reference for design and collaboration tools, demonstrating that PLG can scale past the typical $25M ceiling when the product genuinely supports multi-player workflows.

The 90-day scaling diagnostic

Sarah Chen at $15M ARR needs to know in 90 days whether she is tracking to $50M or stalling. The diagnostic below uses seven structural checks. If three or more fail, the company is heading toward the plateau.

| # | Diagnostic Question | Pass Criteria |

| 1 | Are two or more AEs independently hitting quota for 2+ quarters? | Yes for 2+ AEs |

| 2 | Is NRR above 110%? | Yes (above 110%) |

| 3 | Is the sales team segmented by ACV? | Yes (enterprise / mid / SMB) |

| 4 | Are growth rate + EBITDA margin above 30% combined? | Yes |

| 5 | Is the operating cadence instrumented (WBR + MBR + QBR)? | Yes |

| 6 | Does the leadership team have 4+ functional VPs? | Yes |

| 7 | Are 60% of new bookings from defined ICP? | Yes |

Source: peppereffect 90-day scaling diagnostic, applied to 60+ B2B SaaS audits 2024-2026.

Founders who fail four or more of these have a 14-18 month window to fix the structural issues before the plateau crystallises. Founders who fail six or seven are already plateauing and need an aggressive operating reset within the quarter.

Need a 90-day scaling diagnostic for your SaaS company?

Book a scaling architecture callAI-era scaling: the $10M-$50M cost curve in 2026

AI changes the cost structure of scaling in three ways. First, sales productivity per rep is 30-50% higher with AI-augmented prospecting, qualification, and proposal generation, allowing companies to hit revenue milestones with smaller teams. Second, customer success can manage 2-3x more accounts per CSM through AI-augmented health scoring and proactive outreach. Third, revenue operations runs leaner with AI-driven forecasting, attribution, and pipeline analysis replacing manual analyst work.

The composite effect: AI-native SaaS companies reach $100M ARR in approximately 5.7 years versus the traditional 7.5-7.8 years (Bessemer 2025 benchmarks). ARR per employee runs $500K-$1M for AI-native vendors versus $200K-$400K for legacy. The implication for Sarah Chen is concrete: a company that fails to embed AI into its scaling motion in 2026 will be outrun by a peer that does. The infrastructure investment is modest (under $200K annually at $20M ARR) but the compounding return runs across the entire band.

The 12-month scaling roadmap

A pragmatic 12-month roadmap for a $15M ARR SaaS company targeting $25M.

Months 1-3: stabilise the foundation

Document sales motion. Hire VP Sales if not yet hired. Segment AEs by ACV. Instrument WBR with 8 core metrics. Define ICP precisely. Audit the 7-question diagnostic. Brief board on scaling thesis.

Months 4-6: install the operating system

Hire Head of CS to lead retention motion (target NRR above 115%). Hire Marketing leader to scale demand. Instrument forecasting. Begin SDR hiring. Establish deal desk for ACV above $50K. Run quarterly OKRs.

Months 7-9: scale GTM and refine motion

Add 4-6 AEs across segments. Launch second GTM channel (outbound if PLG, or partnerships if outbound-led). Migrate to tiered pricing. Brief and align board on Stage 3 hiring plan (CRO, CFO).

Months 10-12: prepare for Stage 3

Hire CRO and CFO. Move founder out of in-deal selling. Refresh ICP and pricing. Plan first international or enterprise expansion (if metrics support). Plan capital strategy for next 18 months.

Install the operating system that takes you from $10M to $50M.

peppereffect architects scaling operating systems for $10M-$50M ARR B2B SaaS companies: sales-motion segmentation, NRR engineering, RevOps instrumentation, executive-team design, and an instrumented operating cadence that moves the company from founder-led to executive-led without losing the founder edge. The output is a 12-month roadmap, a measurable Rule of 40 trajectory, and the discipline to defend ICP through the band.

Architect Your Scaling SystemFrequently Asked Questions

What is the SaaS scaling playbook from $10M to $50M ARR?

A SaaS scaling playbook from $10M to $50M ARR is the architectural sequence of organisational, financial, and go-to-market transformations required to move a company from founder-led execution to executive-led predictable growth. It involves five stages (Process Introduction, Functional Specialisation, Executive Layer, Operating-System Maturity, Predictable Growth Machine), eight structural changes, and five disciplines that never change. Only 30% of companies that reach $10M ARR successfully reach $50M within five years.

Why do SaaS companies stall between $10M and $50M ARR?

Approximately 23% of venture-backed B2B SaaS companies plateau in this band. The plateau is rarely a product problem; it is almost always a go-to-market or organisational misalignment. The top three causes are: the founder is still selling beyond their bandwidth, the sales team is generalist when it should be segmented by ACV, and the company is chasing multiple ICPs without dominating one. Founders who diagnose and correct these structural causes within 18 months avoid the permanent plateau.

What is the Rule of 40 at each ARR stage?

The Rule of 40 (growth rate + EBITDA margin should exceed 40%) operates differently at each stage. At $10M-$15M ARR, 40% growth with -20% EBITDA is healthy. At $15M-$25M, 35% growth with -10% margin is healthy. At $25M-$35M, 30% growth with 0% margin. At $35M-$45M, 25-30% growth with 10% margin. At $45M+ ARR, 25% growth with 15% margin becomes the gold standard for a 10x exit multiple. Cutting growth investment too early to manufacture margins is the most expensive mistake.

When should I hire a CRO instead of a VP Sales?

A VP Sales is the right hire at $10M-$15M ARR when the goal is building a repeatable sales motion. A CRO is the right hire at $25M-$35M ARR when the goal is integrating Sales, Marketing, Customer Success, and Revenue Operations under one executive. Hiring a CRO at $15M ARR is premature; the role requires sufficient revenue scale and functional complexity to justify executive overhead. Companies that hire a CRO before $20M ARR typically waste 12-18 months on bureaucracy.

What net revenue retention should I target?

NRR above 110% is the floor at $10M ARR. By $25M ARR, target above 115%. By $50M ARR, target above 120%. Best-in-class SaaS companies achieve 130%+ NRR through disciplined expansion motion: usage-based pricing, expansion sales motion, and quarterly account expansion reviews. NRR above 120% commands premium exit multiples regardless of growth rate.

How much faster do AI-native SaaS companies scale?

AI-native SaaS companies reach $100M ARR in approximately 5.7 years versus 7.5-7.8 years for legacy vendors. ARR per employee runs $500K-$1M for AI-native versus $200K-$400K for legacy. The compounding effect comes from AI-augmented sales productivity (+30-50%), customer success capacity (+2-3x accounts per CSM), and leaner revenue operations. Companies that fail to embed AI in their scaling motion in 2026 will be outrun by AI-native competitors.

When should I expand internationally?

International expansion at $15M ARR is almost always premature. The right timing is typically $25M+ ARR with a dedicated GM, a 12-month investment runway, and at least 15% of inbound pipeline already originating from the target region. Companies that open international offices to chase deals rather than invest in market expansion typically close those offices within 24 months at significant cost.

What is the most expensive scaling mistake?

Premature profit optimisation. Cutting growth investment at $12M-$15M ARR to manufacture 20% EBITDA margins starves the engine that produces exit multiple and signals capped TAM to acquirers. McKinsey's Rule of 40 research documents that this single mistake destroys $30M-$100M in future enterprise value. Run negative margin with confidence through Stage 1-2 if growth is above 35%. compress your sales cycle

Resources

- McKinsey: SaaS and the Rule of 40

- Intelligent Business: Rule of 40 Benchmarks 2026

- Stripe: Net Revenue Retention for SaaS

- FE International: NRR and SaaS Valuation

- ICONIQ Growth: 2025 State of Go-to-Market

- OpenView: 2025 SaaS Benchmarks

- First Round Review: PLG to Enterprise

- David Sacks: The Cadence

- Bessemer: State of the Cloud 2026

- SaaS CFO: Rule of 40 Calculations