The executive search industry entered 2026 as a 63.99 billion USD global market growing at 10.11 percent compound annual growth rate, on track to reach 103.54 billion USD by 2031 according to Mordor Intelligence. The headline number conceals a structural transformation. Retained search dominates with 62.88 percent share but is being reshaped by AI-augmented sourcing infrastructure. Big Five firms (Korn Ferry, Heidrick & Struggles, Spencer Stuart, Russell Reynolds, Egon Zehnder) post mixed performance (Spencer Stuart +17.8 percent, Korn Ferry search +1 percent). PE-backed roll-ups consolidate the mid-market boutique tier. Operating Partner moves and CEO turnover hit record highs. Container/hybrid engagement models grow at 11.72 percent CAGR, the fastest segment in the industry, reshaping the traditional retained versus contingency dichotomy.

This article maps the executive search industry as it stands in 2026: global market size with regional and segment breakdowns, Big Five public company performance with stock and revenue data, the 10 most important industry trends, the disruption threats reshaping the competitive landscape, AI adoption statistics, M&A activity, and the 5 strategic postures search firms are taking to compete in the agentic era. Target audience: managing partners of search firms, fund GPs and talent partners selecting search vendors, CHROs evaluating the supplier landscape, and journalists or investors covering the recruiting industry.

Global Market Size and Growth Trajectory

The retained executive search industry sits inside a broader recruiting market totalling 690.3 billion USD in 2026, growing to 989.32 billion USD by 2031 at 7.47 percent CAGR according to Mordor Intelligence's recruiting market analysis. The executive search segment specifically (defined as retained, contingency, and container search for senior leadership roles) is sized at 58.13 billion USD in 2025 and 63.99 billion USD in 2026, per Mordor's dedicated executive search market report. The 10.11 percent CAGR through 2031 outpaces the broader recruiting market by approximately 3 percentage points.

The growth differential reflects two structural forces. First, demand for senior leadership has tightened as CEO tenure compresses and board succession planning accelerates. The Russell Reynolds Global CEO Turnover Index documents 234 CEO departures globally in 2025, up 16 percent year over year and 21 percent above the 8-year average. Second, the rise of PE portfolio company hiring, with PE/VC-backed client revenue growing at 11.28 percent CAGR according to Mordor, has expanded the addressable market for retained search beyond traditional public company demand.

The corporate and private client mix accounts for 67.12 percent of 2025 executive search revenue. The remaining 33 percent is split between PE/VC-backed clients (fastest-growing segment), nonprofit and education (steady), and government and defence (cyclical). Tech and digital services is the largest vertical at 27.45 percent of search revenue, followed by financial services, healthcare and life sciences (fastest-growing vertical at 10.44 percent CAGR), industrial, and consumer.

| Metric | 2025 | 2026 | 2031 Forecast |

| Global executive search market | $58.13B | $63.99B | $103.54B |

| Implied CAGR 2026-2031 | n/a | n/a | 10.11% |

| US executive search recruiting | $7.35B | ~$7.86B | $10.30B (2030) |

| Broader recruiting market | $642.28B | $690.30B | $989.32B |

Sources: Mordor Intelligence Executive Search Report, NatLaw Review Market Forecast

Regional Distribution: North America Dominant, Asia Pacific Fastest-Growing

North America holds 38.20 percent of the global executive search market in 2025, reflecting the density of Fortune 500 headquarters, the depth of the US private equity ecosystem, and the scale of M&A pipeline. New York remains the #1 global financial centre and the leading hub for retained executive search, with London at #2 anchoring European demand. Europe accounts for approximately 27 to 28 percent of global market share, with Zurich, Frankfurt, Paris, and Amsterdam serving as secondary hubs.

Asia Pacific is the fastest-growing region at 10.71 percent CAGR. The broader APAC recruitment market reached 110.03 billion USD in 2025 with 9.301 percent CAGR forecast through 2033 according to Cognitive Market Research's APAC recruitment analysis. Singapore (#4 GFCI) and Hong Kong anchor APAC retained search demand, with Tokyo, Mumbai, and Sydney as growth markets. Middle East and Africa combined represent approximately 12 to 15 percent of global market share, with the UAE attracting roughly 178,000 skilled professionals in 2025 per BCG's global talent mobility research and Dubai at #6 GFCI. Latin America (Sao Paulo) and emerging African hubs (Morocco, South Africa, Kenya) represent smaller but growing segments.

Global cross-border talent mobility dropped 8.5 percent year over year through August 2025, with approximately 220,000 fewer highly-skilled international relocations than the prior year. The retrenchment reflects tighter immigration policies in the US, UK, and parts of Europe, partially offset by Middle East and APAC inward mobility. The trend has structural implications for cross-border search mandates, which now require deeper visa and relocation expertise than the previous era.

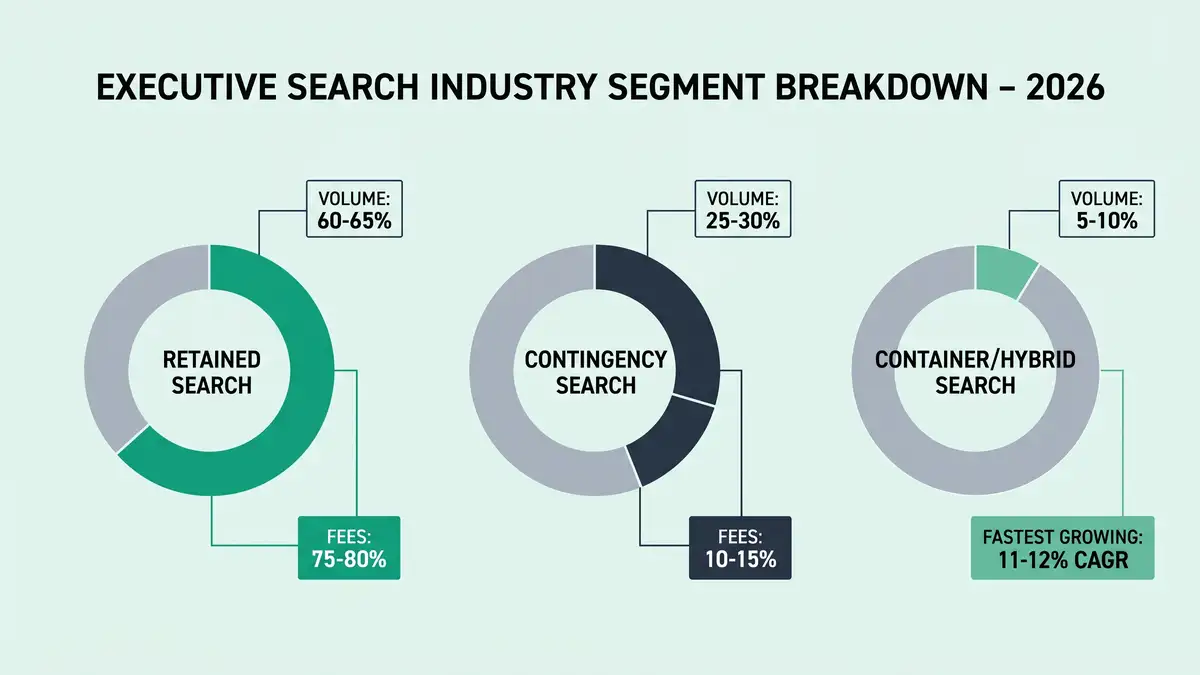

Segment Breakdown: Retained Dominant, Container Fastest-Growing

The retained search segment dominates the executive search industry with 62.88 percent of 2025 revenue, reflecting the structural fit between retained fee economics and C-suite mandate complexity. Industry standard retained fee is 33 percent of first-year compensation (range 25 to 35 percent), billed across the conventional one-third tranche structure documented in our pricing models analysis: one-third on engagement, one-third at shortlist or day 30, one-third on offer acceptance. A typical mid-market CEO search on a 600,000 USD compensation package produces a base fee of 150,000 to 200,000 USD plus ancillaries totalling 220,000 to 300,000 USD all-in (35 to 50 percent effective fee), per PRL International's analysis of 2026 CEO search costs.

Contingency search accounts for approximately 27 to 28 percent of volume but only 10 to 15 percent of fees, reflecting the lower fee-per-mandate economics of contingency engagements at the mid-management level. Container or hybrid engagement models are the fastest-growing segment at 11.72 percent CAGR, with True's SearchEssentials product cited by True Platform's search innovation analysis as a category-defining example of tech-enabled hybrid pricing.

Adjacent markets are reshaping the competitive landscape. Recruitment Process Outsourcing (RPO) reached 9.5 billion USD in 2026 growing to 16.4 billion USD by 2030 at 14.6 percent CAGR according to Mordor, with 62 percent of large organisations using some form of outsourced recruitment and 68 percent of US enterprises using partial or full RPO. The interim and fractional executive segment has expanded sharply: PE operating partner moves between firms tripled to 21 percent of new operating partner hires in 2025 per Hunt Scanlon Ventures' operating partner mobility data, up from 7 percent in 2022.

Big Five Public Company Performance

The Big Five firms control approximately 6 to 8 billion USD of the global retained search fee pool, per Hunt Scanlon Media's Top 50 Executive Search firms ranking, with each operating distinct named assessment methodologies that anchor their premium positioning. Two of the Big Five are publicly traded and disclose detailed financials; three operate as private partnerships with revenues estimated from market intelligence.

Korn Ferry (NYSE: KFY) reported 2.76 billion USD total firm revenue in FY24 with approximately 1.645 billion USD attributable to executive search specifically, per Korn Ferry's investor relations disclosures. The firm posted 4.8 percent revenue growth in Q3 FY26 reaching 708.61 million USD with EPS of 1.28 USD beating consensus of 1.24 USD, per MarketBeat's Korn Ferry earnings analysis. Market cap approximately 8.5 billion USD with P/E of 15.07. Korn Ferry has diversified beyond core retained search into leadership consulting, RPO, and talent assessment which collectively represent approximately 40 percent of total firm revenue.

Heidrick & Struggles (NASDAQ: HSII) reported 1.1 billion USD total FY24 revenue with 769.9 million USD in search fees, per Heidrick & Struggles' Q3 2025 earnings release. Q3 2025 results: net revenue 322.8 million USD up 15.9 percent year over year, Executive Search at 239.1 million USD up 17.0 percent, On-Demand Talent at 50.9 million USD up 10.1 percent, gross margin 89.3 percent, net margin 0.8 percent, 0.15 USD quarterly dividend declared. Market cap approximately 1.2 billion USD with P/E of 30.66 (down from 98.5 at end of 2024).

Spencer Stuart (private) reported 790.1 million USD in 2024 fee revenue, up 17.8 percent year over year, the fastest growth in the Big Five. Spencer Stuart focuses heavily on CEO succession and board advisory practice. Russell Reynolds Associates (private) reported 1.039 billion USD in 2024 fee revenue and owns the influential Global CEO Turnover Index. Egon Zehnder (private partnership) reported 706 million EUR in 2024, per Zehnder Group's 2024 annual report, with strength in financial services, consumer, and industrial verticals.

| Firm | 2024 Revenue | YoY Growth | Structure |

| Korn Ferry (KFY) | $2.76B total / ~$1.645B search | +1% search, +4.8% total Q3'26 | Public, NYSE |

| Russell Reynolds Associates | $1.039B | n/a | Private partnership |

| Heidrick & Struggles (HSII) | $1.1B total / $769.9M search | +7.2% FY24, +15.9% Q3'25 | Public, NASDAQ |

| Spencer Stuart | $790.1M | +17.8% (Big Five leader) | Private partnership |

| Egon Zehnder | $700-800M (EUR 706M) | n/a | Private partnership |

Sources: Hunt Scanlon Top 50 2024, Heidrick Q3 2025 Release, Korn Ferry IR

The 10 Most Important Trends for 2026

AI-augmented sourcing becomes table stakes

Over 60 percent of recruiting teams now use AI in daily workflows producing 66 percent time-to-interview reduction per RecruiterFlow's 2026 AI recruiting analysis. Platforms like HireEZ claim up to 75 percent faster hiring on transactional roles. AI scoring augments but does not replace human consultant judgement at C-suite.

Diversity-balanced shortlists as default standard

AESC member firms commit to gender-balanced and ethnically-diverse shortlists as procurement standard. Clients increasingly include slate-diversity criteria in engagement letters. Washington Technology's diversity progress analysis documents the shift across the federal contractor and Fortune 500 client base.

Embedded recruiter and fractional Talent Partner models

Per Tribe XYZ's embedded recruiter analysis, mid-market companies increasingly engage embedded recruiters (sitting inside the client team as fractional talent partners) rather than transactional retained search. The model captures retained methodology depth at lower fee economics.

Continuous-talent-pipeline retainer models

Search firms increasingly offer continuous-pipeline retainer engagements that maintain pre-qualified candidate networks for predictable future hiring needs, displacing the discrete one-mandate transactional model. The structure aligns with PE portfolio company multi-year hiring cycles.

PE Operating Partner function expansion

Operating partner moves between PE firms tripled to 21 percent of new operating partner hires in 2025 (up from 7 percent in 2022). Operating Partner search has become a dedicated practice line at Big Five firms and PE-specialist boutiques.

ESG and sustainability leadership specialisation

Per Intelligent Employment's ESG executive search analysis, Chief Sustainability Officer, ESG strategy heads, and net-zero transformation leaders represent a discrete and growing search practice. Regulated industries (energy, financial services, manufacturing) drive demand.

Healthcare and life sciences as fastest-growing vertical

10.44 percent CAGR per Mordor, driven by biotech IPO recovery, pharma M&A, and CMO/CSO/CMSO mandate volume. NU Advisory Partners' healthcare talent analysis documents the structural shift.

Cross-border talent mobility complexity

Despite 8.5 percent YoY decline in highly-skilled international relocations, cross-border C-suite search complexity has increased. Visa, tax, and family relocation now require deeper expertise. Search firms with global execution infrastructure differentiate against geography-specific boutiques.

Fractional CXO appointments (CAIO, Head of Data Strategy)

Per Market Rising's fractional leadership analysis, fractional Chief AI Officer and Head of Data Strategy appointments have become standard practice. Search firms now field dedicated fractional-CXO desks running shorter-cycle, higher-velocity mandates.

CEO turnover at record highs

234 CEOs departed globally in 2025 (+16 percent YoY, +21 percent vs 8-year average) per Russell Reynolds Global CEO Turnover Index. The turnover spike has produced record demand for CEO search mandates and elevated the strategic importance of board succession planning practices at the Big Five.

The Disruption Threats

The disruption threats to the executive search industry operate at different layers of the value chain. The most consequential are LinkedIn Recruiter and direct-hire platforms, which have commoditised mid-management sourcing and forced search firms to compete on assessment depth and relationship management rather than candidate identification alone. AI candidate-matching startups (HireEZ, Gem, Plum, Findem) compress sourcing economics further by automating longlist development and initial qualification.

Embedded recruiter platforms (Talentcube, Talent Inc, fractional talent partner networks) attack the retainer model at the mid-market by offering retained-quality methodology at consumption-based pricing. Big consultancies entering search (BCG Vantage, Accenture Talent advisory) compete for leadership advisory revenue rather than search fees directly, but the convergence is increasing. Internal Talent Acquisition function expansion at Fortune 500 enterprises continues to capture VP-level and Director-level mandates that previously routed to retained firms.

The C-suite tier of the market remains structurally protected from these disruption threats because confidentiality (often requiring exclusive mandate structures), off-list referencing depth, board-level relationships, and structured assessment frameworks require human consultant judgement that AI tooling does not replicate. The threats are real at the mid-management layer and increasingly relevant at the VP layer, but the CEO, CFO, board, and PE portfolio CEO mandates continue to consolidate within the Big Five and PE-specialist boutiques.

Big Five versus Boutique Tier Economics

The Big Five and the boutique tier compete on different value propositions. Big Five firms operate global execution infrastructure, deep board-level networks, and brand reputation that justify 32 to 35 percent retainer fees on premium C-suite mandates. AESC's Executive Talent 2025 report documents that 82 percent of business leaders expect search use to increase (30 percent) or hold steady (52 percent), with less than 20 percent expecting a decrease.

Boutique firms differentiate on vertical specialisation depth (PE, healthcare, technology, financial services) or geographic concentration. JM Search reported 21 percent organic year-over-year growth versus the Top 50 average of 11 percent, per Hunt Scanlon's JM Search growth analysis, demonstrating that focused boutiques can outpace Big Five growth in their specialty verticals, a dynamic well documented in our overview of what executive search firms actually do. The boutique tier captures approximately 35 percent of the executive search market with concentration in the 50,000 to 150,000 USD per-mandate fee band that sits below Big Five minimum engagement thresholds.

Architecting the recruiting operating system that compounds placement velocity across your firm's portfolio?

Book a Growth Mapping CallAI Disruption: The 60 Percent Adoption Floor

The adoption of AI in executive search has moved from experimental to operational. Over 60 percent of recruiting teams now use AI in daily workflows, producing measurable productivity outcomes per SHRM's 2026 recruiting priorities research. Time-to-interview compression of 66 percent is the most consistently reported metric. AI is applied across three layers of the search workflow: candidate identification (algorithmic sourcing from LinkedIn, internal CRM, and external databases), screening (AI-assisted resume parsing and initial qualification), and assessment (structured competency mapping against role specifications).

The C-suite tier of the market is the AI-resistant layer. Per RWR's analysis of AI in executive search, the human consultant adds value through off-list reference depth (40 to 60 percent deeper candour than on-list references), board-level relationship management, structured behavioural assessment, integration coaching, and confidentiality protocols. AI augments but does not replace these capabilities at the C-suite tier. The strategic implication for firms is that AI infrastructure is now table stakes for competitive operations, but human consultant depth remains the differentiator at the premium end of the market.

Industry M&A Activity 2024-2026

The executive search industry has seen accelerated M&A activity in 2024-2026 as PE-backed roll-ups consolidate the mid-market boutique tier and Big Five firms acquire leadership advisory practice capabilities. M&A multiples for executive search firms range from 1 to 3x revenue for smaller boutiques (500,000 to 2,000,000 USD revenue) to 4 to 8x EBITDA at scale (3,000,000 USD plus revenue with 20 percent plus net margin). The multiple depends on niche specialisation depth, recurring revenue share, client diversification, retained-search positioning, and recruiter retention. Notable transactions include ZRG Partners' expansion via PE backing, True Search's continued acquisition velocity in the tech and PE verticals, and AMN Healthcare's consolidation moves in the healthcare staffing adjacent market.

The Five Strategic Postures for 2026

Search firms face five distinct strategic postures for the 2026 competitive environment. The choice of posture determines the firm's pricing power, growth ceiling, and vulnerability to disruption threats.

| Strategic Posture | Typical Firm | Pricing Power | Growth Ceiling |

| Premium Retained Specialist (Big Five model) | Korn Ferry, Heidrick, Spencer Stuart | 32-35% retainer + ancillaries | Global scale, $500M-$3B revenue |

| Vertical Sector Specialist | ZRG (PE), JM Search, Nu Advisory (healthcare) | 28-32% retainer, vertical premium | Sector-bounded, $50M-$500M |

| Geography-Specific Boutique | Regional MD-led firms | 25-30% retainer | Regional, $10M-$100M |

| Tech-Enabled Hybrid | True Platform, HireEZ-enabled firms | Container/hybrid pricing, $8-15K + 15-20% | Scalable, $20M-$200M |

| Embedded Fractional Talent Partner | Bespoke, Talentcube, embedded networks | Consumption or monthly retainer | Mid-market, $5M-$50M |

Sources: Direct Recruiters 2026 Trends, Fahrenheit Advisors Strategic Postures

The structural insight

The executive search industry is bifurcating into two distinct competitive zones. The C-suite premium tier remains structurally protected by human consultant depth, off-list referencing, and confidentiality. The mid-management and VP tier is being compressed by AI sourcing, embedded recruiters, and internal TA expansion. Firms attempting to straddle both zones with the same operating model will lose share to firms that pick one and execute it with discipline.

Compensation Across the Industry

Partner-level compensation at Big Five firms typically ranges from 1.5 to 3 million USD plus carry or partnership distributions. Mid-market boutique partners earn 500,000 to 1.5 million USD plus equity in the firm. Senior consultants at retained firms earn 300,000 to 600,000 USD base plus performance bonus. Junior associates and research analysts earn 80,000 to 150,000 USD plus modest bonus. The compensation pyramid is steeper than in management consulting because partner-level fee origination is the primary economic engine.

PE operating partners earn 1.0 to 1.75 million USD cash plus 10 to 60 million USD carry at 25 billion USD plus AUM funds, per Hunt Scanlon Ventures. The compensation differential between PE operating partner roles and senior search firm partner roles has narrowed in recent years as Big Five firms have expanded carry-style structures for their PE practice partners. Global headcount in the executive search profession is estimated at approximately 50,000 search professionals worldwide, concentrated in financial hubs.

Growth Vectors and Threats

The structural growth vectors for the industry through 2030 are: CEO turnover at record highs producing sustained C-suite mandate demand, PE portfolio company hiring at 11.28 percent CAGR, healthcare and life sciences at 10.44 percent CAGR, Asia Pacific at 10.71 percent CAGR, board placement growth as governance scrutiny intensifies, and ESG/sustainability leadership specialisation. The structural threats are: direct-hire platforms commoditising mid-management search, AI tooling compressing sourcing economics, fee compression from procurement-led client engagements, generational shift in client decision-makers favouring tech-enabled boutiques, and macro hiring freezes during recessionary cycles.

The competitive reality

A firm operating in the 2026 executive search industry without dedicated AI infrastructure, vertical specialisation depth, and explicit positioning against Big Five or boutique tier alternatives is structurally vulnerable. The market growth is real (10.11 percent CAGR) but concentrated in firms that have made deliberate strategic choices. Generalist mid-market firms without specialisation depth or technology investment will lose share over the next 5 years.

Architect the operating system that scales your search firm without scaling headcount

Elite executive search firms scaling through the 2026 industry transformation need integrated AI sourcing infrastructure, structured candidate assessment frameworks, MEP compensation expertise, and portfolio-wide relationship management at the operating system level. peppereffect installs the agentic workflows that decouple placement capacity from headcount, automate the 70 percent of manual sourcing work, and protect the AESC-tier methodology that justifies premium retained engagement positioning.

Book a Growth Mapping CallFrequently Asked Questions

How big is the executive search industry in 2026?

The global executive search industry is valued at 63.99 billion USD in 2026 and is forecast to reach 103.54 billion USD by 2031 at a 10.11 percent compound annual growth rate, according to Mordor Intelligence. North America holds 38.20 percent of the market with the US executive search recruiting segment at 7.35 billion USD in 2025 growing to 10.30 billion USD by 2030. Retained search accounts for 62.88 percent of total market share, contingency for 27 to 28 percent, and container/hybrid models capture the fastest-growing segment at 11.72 percent CAGR.

Which are the Big Five executive search firms by revenue?

The Big Five executive search firms by 2024 fee revenue (per Hunt Scanlon Top 50) are Korn Ferry (NYSE: KFY) at approximately 1.645 billion USD in executive search fees within 2.76 billion USD total firm revenue, Russell Reynolds Associates at 1.039 billion USD, Heidrick & Struggles (NASDAQ: HSII) at 769.9 million USD search fees within 1.1 billion USD total, Spencer Stuart at 790.1 million USD (+17.8 percent YoY, fastest-growing Big Five), and Egon Zehnder at 700 to 800 million USD. Korn Ferry and Heidrick & Struggles are publicly traded; the other three are private partnerships.

What are the most important executive search industry trends for 2026?

The most important trends for 2026 are: AI-augmented sourcing (over 60 percent of recruiting teams now use AI daily with 66 percent time-to-interview reduction), diversity-balanced shortlists as default standard, embedded recruiter and fractional Talent Partner models displacing transactional search, continuous-talent-pipeline retainer models, PE Operating Partner function expansion, ESG and sustainability leadership specialisation, cross-border global talent mobility, fractional CXO appointments (Chief AI Officer, Head of Data Strategy now standard), CEO turnover at record highs (234 CEOs departed globally in 2025 per Russell Reynolds Index, +16 percent YoY), and tech-enabled hybrid search models combining AI scoring with human consultant judgement.

Is AI disrupting the executive search industry?

AI is augmenting rather than replacing executive search at the C-suite tier. Over 60 percent of recruiting teams use AI in daily workflows, producing 66 percent reductions in time-to-interview and up to 75 percent faster hiring on transactional roles. AI candidate-matching platforms (HireEZ, Gem, Plum, Findem) and LinkedIn Recruiter Direct Hire have compressed mid-management search economics, but C-suite mandates continue to require human consultant judgement, off-list referencing depth, board-level relationship management, and confidentiality protocols that AI tooling does not replicate. The strategic shift is from reactive sourcing to proactive continuous-pipeline talent strategy enabled by AI infrastructure.

What is the fastest-growing segment of the executive search market?

Container and hybrid engagement models are the fastest-growing segment at 11.72 percent CAGR, expanding faster than both retained (60 to 65 percent of market) and contingency (25 to 30 percent of market) models. Asia Pacific is the fastest-growing geography at 10.71 percent CAGR with the broader APAC recruitment market reaching 110.03 billion USD in 2025. Life sciences and healthcare is the fastest-growing vertical at 10.44 percent CAGR. PE/VC-backed client revenue is expanding at 11.28 percent CAGR as private equity portfolio companies become a larger share of executive search demand.

How are public executive search companies performing?

Korn Ferry (NYSE: KFY) trades at approximately 8.5 billion USD market cap with P/E of 15.07, reported 4.8 percent revenue growth in Q3 FY26 reaching 708.61 million USD, and EPS of 1.28 USD beating consensus 1.24 USD. Heidrick & Struggles (NASDAQ: HSII) trades at approximately 1.2 billion USD market cap with P/E of 30.66, reported 15.9 percent net revenue growth in Q3 2025 reaching 322.8 million USD with Executive Search at 239.1 million USD (+17.0 percent) and On-Demand Talent at 50.9 million USD (+10.1 percent). Both stocks have underperformed S&P 500 over the trailing 12 months but show strong fundamental growth in their executive search practices.

How is private equity affecting the executive search industry?

Private equity is driving structural change in the executive search industry through portfolio company talent strategy, Operating Partner function expansion, and PE-backed roll-ups of mid-market search firms. PE/VC-backed clients now grow at 11.28 percent CAGR, faster than the overall market. PE operating partner moves between firms tripled to 21 percent of new operating partner hires in 2025 (up from 7 percent in 2022). Operating Partners at 25 billion USD AUM funds earn 1.0 to 1.75 million USD cash plus 10 to 60 million USD carry. The PE talent function has become a primary growth vector for both Big Five firms (Korn Ferry, Heidrick PE practices) and PE-specialist boutiques (ZRG Partners, True Search, Notch Partners).

Resources

- Mordor Intelligence: Executive Search Market Report

- Mordor Intelligence: Recruiting Market Report

- NatLaw Review: Executive Search Market 2026-2030 Forecast

- Hunt Scanlon: Top 50 Executive Search Firms Ranking

- AESC: Executive Talent 2025 State of the Industry

- Korn Ferry: Investor Relations Disclosures

- Heidrick & Struggles: Q3 2025 Earnings Release

- MarketBeat: Korn Ferry Earnings Analysis

- Egon Zehnder: 2024 Annual Report

- HR Executive: Russell Reynolds CEO Turnover Index 2025

- Hunt Scanlon Ventures: Operating Partner Mobility 2025

- PRL International: CEO Search Cost Analysis 2026

- True Platform: SearchEssentials Hybrid Pricing

- Cognitive Market Research: APAC Recruitment Market Report

- BCG: Global Talent Mobility Shifts 2025

- RecruiterFlow: AI Recruiting in 2026

- RWR: Will AI Replace Executive Recruiters

- SHRM: Recruiting Priorities 2026 Research

- Intelligent Employment: ESG Executive Search 2026

- NU Advisory Partners: Healthcare Talent 2026

- Tribe XYZ: Embedded Recruiters 2026 Analysis

- Market Rising: Fractional Leadership Analysis

- Washington Technology: Diversity Progress Executive Search

- Direct Recruiters: 2026 Industry Trends

solo to scale boutique practice building economics search firm KPI benchmarks and dashboards candidate sourcing strategies for 2026 recruitment process outsourcing market dynamics inbound mandate marketing playbook EBITDA margins and revenue per recruiter benchmarks scaling from 5 to 50 consultants without losing culture partnership model for executive search client relationships niche vs generalist positioning decision