Private equity has shifted decisively from financial engineering to operational value creation, and talent strategy has moved with it. Over 70 percent of PE returns now come from operational improvement rather than leverage and multiple expansion, according to Bain's analysis, which means the executive who runs the portfolio company is no longer a supporting cast member to the investment thesis. The portco CEO, CFO, and operating partner are the investment thesis. Executive search for private equity is therefore not a vendor management exercise. It is the operational infrastructure that determines whether a 5 to 7 year hold cycle produces top-quartile returns or median fund performance.

This article decodes how PE executive search actually works: the six-phase deal-aligned search process that runs parallel to deal diligence rather than sequentially, the three distinct executive roles PE firms hire (operating partner, portco CEO, portco CFO) with their compensation architectures, the Management Equity Plan (MEP) structures that align incentives across hold periods, the Big Five PE practices and PE-specialist boutique alternatives, the talent strategy patterns by fund type (megafund, mid-market, lower mid-market, family office, growth equity), and the 7-question diligence framework that PE talent partners should run before granting any search mandate. The objective is to install the talent procurement discipline that protects the 200 to 300 basis points of IRR uplift that strong portco leadership produces, building on the broader principles documented in our guide to what executive search firms actually do.

The PE Talent Imperative: Why Portfolio Company Leadership Is the Investment Thesis

The economics of modern private equity have inverted relative to the leverage-driven era of the 1990s. Operational improvement now accounts for over 70 percent of PE returns, up from approximately 35 percent three decades ago, according to Bain's 2026 Global Private Equity Report. Multiple arbitrage and financial engineering produced returns when interest rates were structurally falling and EBITDA multiples were structurally rising. Neither dynamic is operative in 2026. The funds generating top-quartile returns are the ones whose portfolio companies execute operational value creation playbooks under disciplined leadership.

This shift makes the portco CEO appointment the single most consequential post-close decision a deal team makes. Industry research suggests that approximately 45 percent of portfolio company CEOs are replaced within 18 months of acquisition, most commonly because the original CEO lacks the leveraged-environment experience or operational tempo required to execute the value creation thesis. Each replacement costs the fund 1.5 to 2.0 percent of equity value per month of leadership vacancy, plus the disruption cost of restarting the 100-day plan. HSIQ Talent Intelligence's analysis of Bain's 2026 PE report documents that talent risk has moved to the centre of investment committee discussions, with leading funds installing structured talent diligence parallel to commercial and financial diligence.

The compounding effect is that PE funds with structured talent strategies and dedicated operating partners generate 200 to 300 basis points of additional net IRR over fund life relative to peers without such infrastructure. That uplift translates to 15 to 20 percent of potential fund returns at stake based on the quality of portco leadership and the speed of post-close talent execution. Talent strategy is therefore not a procurement function. It is an alpha source.

The Three PE Executive Roles Decoded

PE firms hire three distinct executive profiles, each with different compensation architectures, search methodologies, and value creation mandates. Confusing them produces hiring failures and misaligned incentives.

The Operating Partner is a full-time PE firm employee, not a portfolio company employee. Operating Partners typically manage 1 to 3 portcos concurrently as active board members and operational advisors. Compensation ranges from 400,000 USD to over 2 million USD annually, structured as base salary plus performance bonus plus often carried interest participation in the fund. The Operating Partner model was pioneered by Bain Capital, KKR Capstone, and Carlyle in the 2000s and has since expanded across mid-market funds. Private Equity International's annual Operating Partners Human Capital Forum tracks the function's expansion across the industry.

The Portfolio Company CEO is a full-time portco employee, equity-rich and fully aligned with the investment thesis. Base salary ranges from 400,000 to 1.5 million USD depending on portco size and industry. The CEO receives 1 to 5 percent of company equity through a Management Equity Plan (MEP), plus a 1.0 to 1.5x base salary cash bonus tied to IRR hurdles. Total compensation opportunity at exit can exceed 5x to 10x annual cash compensation in successful holds. The CEO must execute the value creation plan, manage the dense PE board governance cadence (monthly to bi-weekly meetings versus quarterly public company boards), and prepare the company for exit through IPO, strategic sale, or secondary buyout.

The Portfolio Company CFO is the second strategic hire after the CEO and arguably the more difficult search because the candidate pool is narrower. Base salary ranges from 250,000 to 600,000 USD, with total cash compensation of 400,000 to 900,000 USD. The CFO receives 0.5 to 2.0 percent MEP equity plus a 0.75 to 1.0x base bonus. The CFO must be capable of leading the company through IPO preparation, S-1 drafting, audit readiness, or strategic sale due diligence depending on the exit thesis. Industry research suggests only about 30 percent of CFO candidates have genuine exit preparation experience, which makes the CFO search the most market-constrained mandate in the PE search portfolio.

Why PE Funds Use Specialist Executive Search Firms

The speed and resource intensity of PE executive search is structurally different from corporate search, which is why generalist firms underperform on PE mandates. According to Christian & Timbers' 2026 PE recruiter rankings analysis, specialist PE search practices complete C-suite mandates in 60 to 90 days compared to 120 to 180 day corporate search timelines. The compression is critical because every week of post-close leadership vacancy erodes 1 to 2 percent of equity value through stalled operational execution.

The speed advantage comes from four sources. First, specialist firms maintain pre-curated networks of executives who have done it before, with full diligence already completed on PE-fit dimensions (leverage comfort, board governance experience, 100-day plan track record). Second, specialist firms run confidential post-LOI sourcing parallel to deal diligence rather than waiting for close. Third, specialist firms have structured value-creation-plan assessment frameworks that compress candidate evaluation. Fourth, specialist firms are integrated into the deal team workflow, attending IC meetings and adjusting search direction in real time as deal terms evolve.

Confidentiality is the other dimension where specialist firms differentiate. PE mandates require operating under NDA during the pre-close phase, with shortlists that cannot leak to portfolio company employees, competitors, or the public market. MSH Talent's analysis of top PE search firms identifies that 78 percent of PE firms rate confidentiality as the single most critical factor when selecting search partners for pre-close mandates.

Speed equals IRR

A portco where the CEO is named, signed, and operational on day one of close versus day 90 of close represents an IRR delta of approximately 50 to 100 basis points across the hold period. Specialist PE search firms exist to compress that timeline. Generalist firms running a sequential post-close search are leaving alpha on the table by design.

The Big Five PE Practices and Specialist Boutiques

The PE executive search market splits between the Big Five global firms with dedicated PE practices and a specialist boutique tier that captures approximately 35 percent of the market. Each tier serves different fund segments and search profiles.

The Big Five PE practices are Heidrick & Struggles (PE practice generates over 200 million USD in annual revenue), Korn Ferry, Spencer Stuart, Russell Reynolds Associates, and Egon Zehnder. Each firm operates a dedicated PE practice with practice partners, specialist consultants, regional teams, and pre-curated candidate networks. The Big Five dominate megafund and large mid-market searches where global reach, brand reputation, and depth of board-level methodology matter most.

The PE-specialist boutique tier includes ZRG Partners (PE-owned itself), True Search, Caldwell Partners, DHR Global, and Notch Partners. These firms compete on PE-specific specialisation depth, faster turnaround, and more favourable pricing structures for mid-market and lower-mid-market funds. Bespoke Partners, identified in their 2025 PE Talent Trends analysis, represents the next-generation PE search boutique focused on data-driven candidate matching and accelerated search timelines.

| Firm Tier | Typical Fund Segment | Retainer Fee | Minimum Engagement |

| Big Five PE practice | Megafund and large mid-market | 33-40% (PE premium) | $150K-$300K |

| PE-specialist boutique tier 1 | Upper mid-market | 30-35% (see pricing breakdown) | $120K-$200K |

| PE-specialist boutique tier 2 | Lower mid-market | 28-32% | $80K-$150K |

| Generalist with PE practice | Family office, independent sponsor | 25-30% | $60K-$120K |

Sources: Christian & Timbers PE Recruiter Rankings 2026, Talentfoot Top PE Executive Search 2026

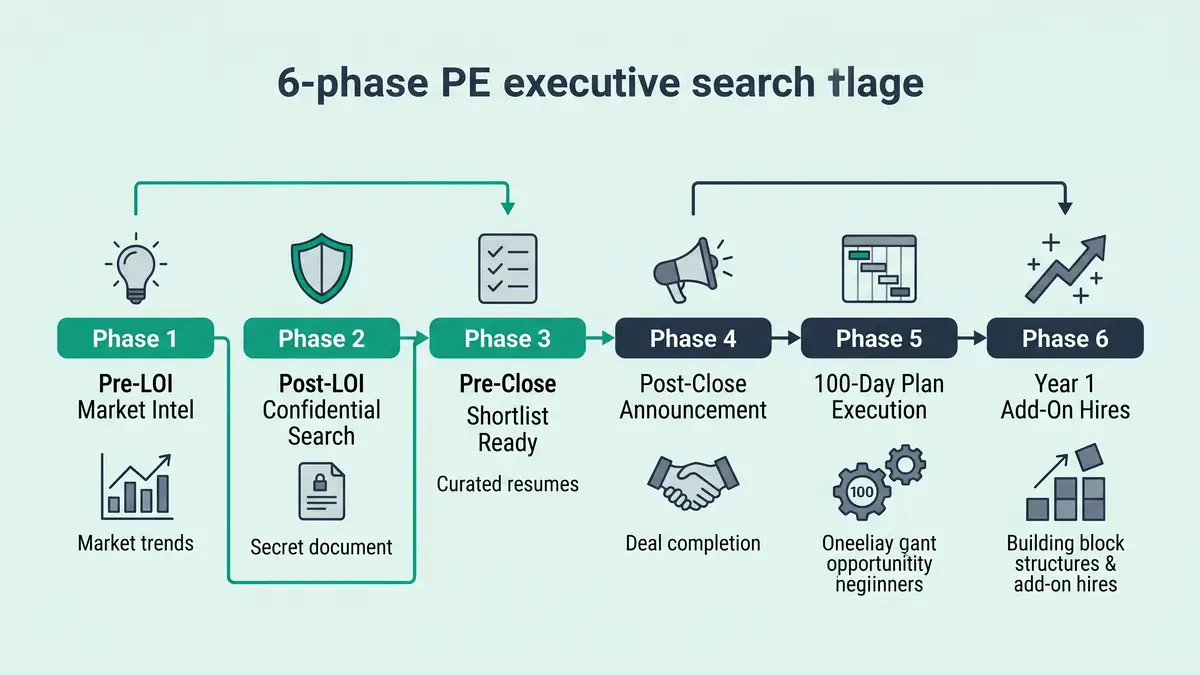

The 6-Phase PE Search Process

PE executive search runs in six deal-aligned phases rather than the sequential post-close model that defines corporate search. The phase structure reflects the reality that talent risk has to be diligenced and resolved in parallel with commercial and financial diligence, not afterward.

Pre-LOI: Talent Landscape Mapping

Search firm runs talent landscape mapping and compensation benchmarking parallel to deal sourcing diligence. Outputs include sector-specific executive availability, competitor talent depth, and MEP benchmarking. Industry research suggests this phase reduces post-acquisition CEO replacement by approximately 28 percent because the deal team enters LOI with talent risk already assessed.

Post-LOI: Confidential Search Under NDA

Discreet candidate identification, structured assessment, and reference work under NDA. PE-specific competency assessments produce 32 percent higher leadership success rates than generalist competency models. Shortlist of 3 to 5 candidates ready for board interview within 30 to 45 days. Speed matters because each week of post-close delay erodes approximately 0.8 to 1.2 percent of equity value.

Pre-Close: Final Selection and MEP Structuring

Board interviews, final candidate selection, MEP negotiation, and offer extension. Optimised MEP structures aligned with deal economics produce approximately 25 percent higher executive retention through the hold period. Pre-close offer execution under exclusive mandate terms allows day-one operational continuity.

Post-Close: Announcement and Onboarding

Coordinated CEO announcement to portfolio company, key stakeholders, and market. 30-day intensive onboarding with the deal team, operating partner, and incumbent leadership. Search firm transitions from execution mode to integration support mode.

100-Day Plan Execution

CEO leads execution of the value creation plan agreed pre-close. The first 100 days account for approximately 62 percent of value creation leverage in the hold period. Search firm provides ongoing executive coaching and CFO/COO hiring support as add-on mandates surface.

Year One Add-On Hires

CFO recruitment if not paired with CEO at close, COO or Chief Revenue Officer additions, and functional VP build-out as the value creation plan progresses. Search firm operates as outsourced talent function for the portco's first full year under PE ownership.

Management Equity Plan (MEP) Compensation Architecture

The Management Equity Plan is the compensation infrastructure that aligns portco executive incentives with fund return objectives. The structure differs materially from public company equity compensation because PE compensation is tied to absolute equity value at exit rather than to share price appreciation in a continuously priced market. The MEP architecture defines the alpha that the executive search firm sells.

| Tier | Role | MEP Equity | Cash Bonus | Vesting |

| Tier 1 | Portfolio Company CEO | 1-5% | 1.0-1.5x base | 4-year + exit acceleration |

| Tier 2 | Portfolio Company CFO | 0.5-2% | 0.75-1.0x base | 4-year + exit acceleration |

| Tier 3 | Functional VPs (CRO, COO, CTO) | 0.25-0.5% | 0.5x base | 4-year cliff structure |

| Tier 4 | Director-level functional leaders | 0.1-0.25% | 0.25-0.5x base | 4-year cliff structure |

Source: Recruiting Excellence Center Specialized PE Recruiting Report

MEP equity typically vests over 4 years with acceleration on exit, meaning the executive retains unvested equity if the fund achieves a successful exit before the 4-year cliff completes. Hurdle rates and waterfall mechanics determine the equity payout structure: most MEPs require the fund to return 2x to 3x invested capital before the executive equity becomes meaningfully valuable, with disproportionate upside above the hurdle. This structure aligns the executive with fund IRR rather than with portco revenue or EBITDA growth in isolation.

Architecting the recruiting operating system that compounds placement velocity across PE portfolio company mandates?

Book a Growth Mapping CallTalent Strategy by PE Fund Type

The talent strategy that suits a 50 billion USD megafund differs structurally from the strategy that suits a 500 million USD lower-mid-market fund. Fund size, hold thesis, sector concentration, and operational model all shape the optimal search partner mix.

Megafunds (Blackstone, KKR, Apollo, Carlyle, CVC, Advent, EQT) operate large in-house operating partner teams and dedicated talent partner functions. KKR Talent Partners, Bain Capital Talent, and Apollo Human Capital are full-time internal functions that manage executive networks, OP-CEO matching, and cross-portfolio talent strategy. Megafunds use Big Five PE practices for specific high-profile searches but execute substantial volume internally. Average internal talent function headcount: 15 to 40 professionals per megafund.

Upper mid-market funds (1 to 5 billion USD) operate hybrid models with smaller in-house talent teams of 3 to 8 professionals plus heavy reliance on Big Five and specialist boutique PE practices. The talent partner reports to the Head of Portfolio Operations or Managing Partner and coordinates search firm selection across the portfolio.

Lower mid-market funds (300 million to 1 billion USD) typically operate without dedicated in-house talent partner functions. Talent is managed at the deal partner level with full outsourcing to retained PE search specialists. Retained search dominates at this tier because the fund cannot economically build internal talent infrastructure.

Family offices and independent sponsors outsource the talent function entirely, often to PE-specialist boutiques that operate as fractional talent partners across multiple sponsor relationships. Underdog.io's analysis of PE recruiter selection identifies that this segment increasingly demands integrated talent infrastructure rather than transactional search execution.

Growth equity funds focus on VP and Director-level talent rather than CEO replacement because the founder typically remains in seat. Search firms operating in growth equity look more like late-stage executive search than traditional buyout talent strategy, with emphasis on scaling functional infrastructure rather than installing turnaround leadership.

The 7-Question Diligence Framework for PE Search Firm Evaluation

Before granting a search mandate to any PE firm, the talent partner or deal team should run a structured 7-question diligence framework. The framework forces every dimension of the firm's PE capability onto an explicit evaluation grid. Firms that cannot answer all seven with specifics are not operating at the PE specialist tier required for portfolio company mandates.

What is the firm's PE practice depth, headcount, and revenue concentration?

Big Five firms should disclose dedicated PE practice headcount (typically 30 to 80 consultants), practice partner names, and PE revenue as a share of total firm revenue (Heidrick PE practice exceeds 200 million USD annually). Boutiques should disclose PE share of total mandates (target 60 percent or above).

What is the candidate pool depth and OP-CEO matching capability?

Specialist firms maintain pre-curated networks of PE-fit executives with full diligence on leverage comfort, board governance experience, and 100-day plan track record. Demand specific examples of OP-CEO pairing successes and named candidate density by sector and geography.

What is the firm's exit preparation experience?

Demand named examples of CEO and CFO placements that successfully led portcos through IPO, strategic sale, or secondary buyout. Verify the firm has placed executives across the full exit lifecycle, not just at deal close. Approximately 30 percent of CFO candidates have genuine exit preparation experience; the firm must show how it identifies and qualifies the 30 percent.

What is the firm's MEP compensation expertise?

The search firm should provide structured benchmarking on MEP equity tiers, cash bonus multiples, vesting structures, hurdle rates, and waterfall mechanics by sector and deal size. Reject firms that cannot articulate the compensation architecture or that defer MEP structuring to the fund's legal counsel without contribution.

What is the firm's confidentiality and NDA-compliant process?

Pre-close mandates require strict NDA-compliant sourcing, redacted shortlist presentation, and discreet reference protocols that protect deal confidentiality. Demand documentation of the firm's pre-LOI and post-LOI confidentiality procedures. 78 percent of PE firms rate confidentiality as their most critical search firm selection factor.

What is the firm's timeline commitment and milestone discipline?

Specialist firms commit to 30 to 45 day shortlist and 60 to 90 day total search timelines. Demand explicit timeline commitments in the engagement letter with milestone-based termination rights if the firm misses targets. Generalist firms operating 120-day timelines are not PE-fit.

What is the firm's post-placement integration and add-on hiring capability?

The CEO placement is the first hire, not the only hire. Specialist firms support post-placement onboarding, 100-day plan coaching, and year-one CFO/COO/CRO add-on mandates as an integrated service rather than as separate engagement letters. Confirm the firm's bench depth to handle the full hold-period talent strategy, not just the initial mandate.

Common Mistakes PE Firms Make in Portfolio Company Search

PE deal teams operating without specialist talent infrastructure make characteristic mistakes that the diligence framework above is designed to prevent.

The first is treating PE search like corporate search by waiting until post-close to begin sourcing. Sequential post-close search costs 60 to 90 days of value erosion. The PE-fit alternative is parallel post-LOI confidential sourcing under NDA, with shortlist ready at close. The second is withholding exit timeline and thesis from the search firm. The CEO who suits a 3-year flip differs structurally from the CEO who suits a 7-year platform build. The third is underweighting cultural fit with the dense PE board governance model. Many publicly successful CEOs cannot adapt to monthly board meetings, weekly operating partner calls, and continuous MD-level engagement, and the cultural mismatch produces 18-month exits.

The fourth mistake is skipping structured management assessment. PE-fit assessment frameworks surface leverage comfort, value-creation-plan execution capability, and 100-day plan mastery in ways that unstructured interview cycles do not. The fifth is inadequate MEP structuring at offer stage. A poorly structured MEP produces misaligned incentives that destroy hold-period value, while an optimally structured MEP produces 25 percent higher executive retention through exit. The sixth is treating the search as transactional rather than as a multi-year talent partnership. The CEO is the first hire; the CFO, COO, CRO, and functional VPs follow over 12 to 18 months. Funds that engage search firms transactionally for each role pay more in aggregate and lose the integration advantage of a single partner managing the full talent build.

The cost of talent failure

A failed portco CEO appointment costs the fund 200 to 400 basis points of net IRR across the hold period, plus the disruption cost of restarting the value creation plan. The 60 to 100 basis point fee differential between a Big Five specialist and a generalist firm is irrelevant in this risk envelope. Procurement optimisation at the executive search line is a structurally bad trade for any fund operating at scale.

Architect the recruiting operating system that scales placement velocity across PE portfolios

Elite PE-specialist executive search firms scaling beyond founder-led delivery need an integrated operating system across mandate qualification, deal-stage sourcing, structured assessment, MEP structuring, and portfolio-wide candidate relationship management. peppereffect installs the agentic workflows that decouple placement capacity from headcount, automate the 70 percent of manual sourcing work, and protect the AESC-tier methodology that justifies premium PE practice positioning.

Book a Growth Mapping CallFrequently Asked Questions

What is executive search for private equity?

Executive search for private equity is the discipline of identifying, assessing, and placing C-suite leaders into portfolio companies acquired by PE funds, with engagement structures aligned to the deal lifecycle (pre-LOI mapping, post-LOI confidential search, pre-close shortlist, post-close announcement, 100-day plan execution, year-one add-on hires). PE searches are typically completed in 60 to 90 days versus 120 to 180 days for corporate searches, and require specialist firms with deep PE network depth, value-creation-plan assessment capability, MEP compensation expertise, and exit-preparation experience.

Why do PE firms use specialist executive search firms?

PE firms use specialist search firms because portfolio company leadership requires distinct capabilities that generalist corporate searches do not surface: value-creation-plan execution, comfort with leverage and dense PE board governance, 100-day plan mastery, IRR-aligned decision making, and exit preparation experience. Specialist PE practices at Heidrick, Korn Ferry, Spencer Stuart, Russell Reynolds, and Egon Zehnder, plus boutiques like ZRG Partners and True Search, maintain pre-curated networks of PE-fit executives who have done it before, enabling 60-to-90 day searches versus 120-to-180 day corporate timelines.

How much equity does a portfolio company CEO receive?

A portfolio company CEO typically receives 1 to 5 percent of company equity through a Management Equity Plan (MEP) structure, alongside a base salary of 400,000 to 1.5 million USD and a cash bonus of 1.0 to 1.5x base salary tied to IRR hurdles. Vesting is typically 4 years with acceleration on exit. The CEO MEP allocation represents 75 to 100 percent of total compensation opportunity tied to value creation, aligning incentives with fund returns and the 5 to 7 year hold period.

What is an Operating Partner at a PE firm?

An Operating Partner is a full-time PE firm executive who serves as an active board member and operational advisor to multiple portfolio companies, typically managing 1 to 3 portcos concurrently. Operating Partners earn 400,000 USD to over 2 million USD annually in base salary plus performance bonus plus often carried interest participation. The role was pioneered by Bain Capital, KKR Capstone, and Carlyle, and has expanded across mid-market funds. Operating Partners drive value creation plan execution, support portco CEO transitions, and coordinate cross-portfolio talent strategy.

How long does a private equity executive search take?

A specialist private equity executive search typically completes in 60 to 90 days from engagement to candidate start date, compared to 120 to 180 days for corporate executive searches. Speed differential is driven by pre-curated PE-fit candidate networks at specialist firms, parallel post-LOI confidential sourcing during deal diligence, structured value-creation assessment frameworks, and deal-team integration that compresses interview cycles. The 60 to 90 day window is critical because every week of post-close leadership vacancy erodes equity value at approximately 1 to 2 percent per month.

What are the Big Five PE executive search practices?

The Big Five PE practices are Heidrick & Struggles, Korn Ferry, Spencer Stuart, Russell Reynolds Associates, and Egon Zehnder. Heidrick's PE practice generates over 200 million USD in annual revenue. Each firm operates a dedicated PE practice with practice partners, specialist consultants, and pre-curated candidate networks across geographies. Big Five firms compete with PE-specialist boutiques including ZRG Partners (PE-owned itself), True Search, Caldwell Partners, DHR Global, and Notch Partners, which collectively capture approximately 35 percent of the PE executive search market.

What is the difference between a portco CEO search and a public company CEO search?

A portco CEO search prioritises value-creation-plan execution, comfort with leverage and dense PE board governance, 100-day plan mastery, IRR-aligned compensation structures, and exit preparation experience over the growth-at-all-costs profile of public company CEOs. PE-owned boards have 5 to 7 highly engaged investment professionals (versus 8 to 12 generalist public co directors) and meet monthly to bi-weekly. The portco CEO must execute the investment thesis under compressed 5 to 7 year hold periods with 200 to 300 basis points of IRR uplift attributable to leadership effectiveness in the first 100 days.

Resources

- Bain & Company: Welcome to a New Era Global Private Equity Report 2026

- Bain & Company: Global Private Equity Report 2026 Hub

- HSIQ Talent Intelligence: Bain Disciplined Era PE Talent Risk Analysis

- Christian & Timbers: Top Private Equity Recruiters 2026 Rankings

- Talentfoot: Top Executive Search Firms for Private Equity 2026

- MSH Talent: Top 7 Private Equity Executive Search Firms 2026

- Recruiting Excellence Center: Specialised Private Equity Recruiting Report

- M&A Community: Top Private Equity Recruiting Firms

- PEI: Operating Partners Human Capital Forum 2026

- Underdog.io: Top 10 Private Equity Recruiters Analysis

- Nexus IT Group: Top 10 Private Equity Recruiters

- Cowen Partners: Private Equity Executive Search

- Bespoke Partners: Private Equity Talent Trends 2025

- hireneXus: Top Private Equity Executive Search Firms

executive search industry landscape executive search industry landscape and Big Five performance BD playbook for partnership channels with PE firms portfolio succession planning advisory service PE portfolio healthcare executive search