The default assumption among first-time SaaS founders is that raising venture capital is what serious companies do. The 2026 data says otherwise. Bootstrapped B2B SaaS companies in the $3M to $20M ARR range now post 103% median NRR, 90%+ gross margins, and 15% annual growth while founders retain 70-100% of equity. Venture-backed peers grow faster on average, but Series B and C rounds in 2026 are harder to close, take longer, and dilute founders 50-65% by the time the company reaches $50M ARR. The question is no longer "should I raise?" The question is which capital structure produces the highest-probability founder-aligned outcome at your specific stage.

This article installs the seven-question diagnostic Sarah Chen needs to make that decision in 2026. It covers the 2026 funding environment, the bootstrap economics that have shifted in the AI-native era, dilution math through Seed to Series C, hybrid paths (venture debt, revenue-based financing, secondary tender), and the 30/60/90-day implementation plan for either route. The framework interlocks with our broader SaaS growth strategy playbook and scale-revenue-without-headcount framework, which often determines whether the venture math is even necessary.

Strategic intent

Bootstrap and venture are capital instruments, not identities. The right one depends on market structure, capital intensity, founder ownership goal, and outcome range. Pick the wrong instrument and the company architecture follows the capital instead of the strategy.

The 2026 Funding Environment

Three things changed between 2022 and 2026. First, the bar for Series B and C rose materially. Median time to close a Series B in 2026 sits at six to nine months, double the 2021 norm. Investors expect $5M+ ARR with 80%+ growth, sub-15-month CAC payback, and Rule of 40 above 40 before serious term-sheet conversations begin (High Alpha 2026 Fundraising Data). Second, AI-native companies absorbed most of the available capital in 2025-2026, leaving traditional SaaS rounds smaller and slower. Third, the secondary market for founder liquidity matured, removing one of the historical reasons founders raised primary capital (cashing out personally).

The bootstrap side improved in parallel. AI-native operations compressed the cost to reach $1M ARR by an estimated 40-60% versus the 2020 baseline. Top-quartile bootstrapped SaaS now reach $1M ARR in 2 years, just 4 months slower than the average VC-backed company (Wellows 2026). At $3M-$20M ARR, the median bootstrapped company posts 103% NRR with 90%+ gross margin and runs cash-flow positive (SaaS Capital 2026). The structural advantage of venture (capital to outpace competitors) is therefore narrower in 2026 than at any point in the last decade for most non-winner-take-most categories.

The Dilution Math: What You Actually Keep

The single most under-modelled variable in raise-vs-bootstrap is what the founder personally takes home at exit. The math works out very differently across the three common paths.

| Path | Founder ownership at $100M exit | Founder ownership at $500M exit | Founder ownership at $1B exit | Typical exit timeline |

| Pure bootstrap (no outside capital) | 70-100% | 70-100% | 70-100% | 8-15 years |

| Hybrid (small angel + venture debt + RBF) | 55-75% | 55-75% | 55-75% | 7-12 years |

| Standard venture (Seed + A + B + C) | 15-25% | 15-25% | 15-25% | 7-10 years |

| Heavy venture (mega rounds, multiple primary) | 5-15% | 5-15% | 5-15% | 8-12 years |

Source: Carta State of Private Markets 2025-2026, Index Ventures Founder Sharing Survey.

The bootstrap founder at a $100M exit takes home roughly the same dollar value as a heavy-venture founder at a $1B exit. That is the number the founder needs to internalise before deciding which path optimises for their actual goal. For most $10M-$40M ARR B2B SaaS, the realistic exit range is $50M-$300M, which means the bootstrap path produces meaningfully better personal outcomes unless the company is in a winner-take-most market with billion-dollar trajectory.

The 4 Pillars Playbook breaks down the entire framework with deployment maps, KPIs, and real case studies across SaaS, recruiting, and coaching.

Open the Interactive PlaybookThe Capital-Intensity Test: When Venture Is Actually Required

Venture capital is structurally required in a small set of conditions. Outside those conditions, raising primary equity is a choice, not a requirement, and the choice has consequences.

The four conditions that create a structural venture requirement are: winner-take-most market dynamics where first-mover scale produces lasting moats (LinkedIn, Salesforce in their categories); capital-intensive GTM where enterprise sales motion costs $5M-$15M to bootstrap before unit economics work; capital-intensive product where engineering, infrastructure, or hardware capex exceeds $5M before revenue traction is possible; and geographic land-grabs where multi-continental simultaneous expansion is a strategic requirement.

For most vertical SaaS, niche tools, prosumer SaaS, profitable B2B SaaS in fragmented markets, and developer tools, none of these four conditions hold. Founders should validate market structure first using a tight B2B SaaS benchmark comparison before deciding the capital path. The market is large but fragmented. Three to seven competitors will reach $50M-$200M ARR each, and the founder who keeps 70% of the company at a $200M exit takes home more than the founder who kept 15% at a $1B exit (Bessemer Atlas 2026).

Bootstrap vs Venture: 2026 Economic Profile

| Metric | Bootstrapped SaaS | Venture-backed SaaS |

| Median ARR growth | 15-25% | 30-60% |

| Median NRR | 103% | 110-120% |

| Gross margin | 90%+ | 75-85% |

| FCF margin | +25 to +40% | -30 to +5% |

| Rule of 40 | 35-50% | 40-60% |

| Burn Multiple | n/a (cash positive) | 0.8-2.0x |

| Founder ownership at $100M exit | 70-100% | 15-25% |

| Survival rate to 5 years | ~50% | ~30-40% |

Source: SaaS Capital 2026 Bootstrapped Benchmarks, OpenView 2025 SaaS Benchmarks, ICONIQ 2025 State of GTM.

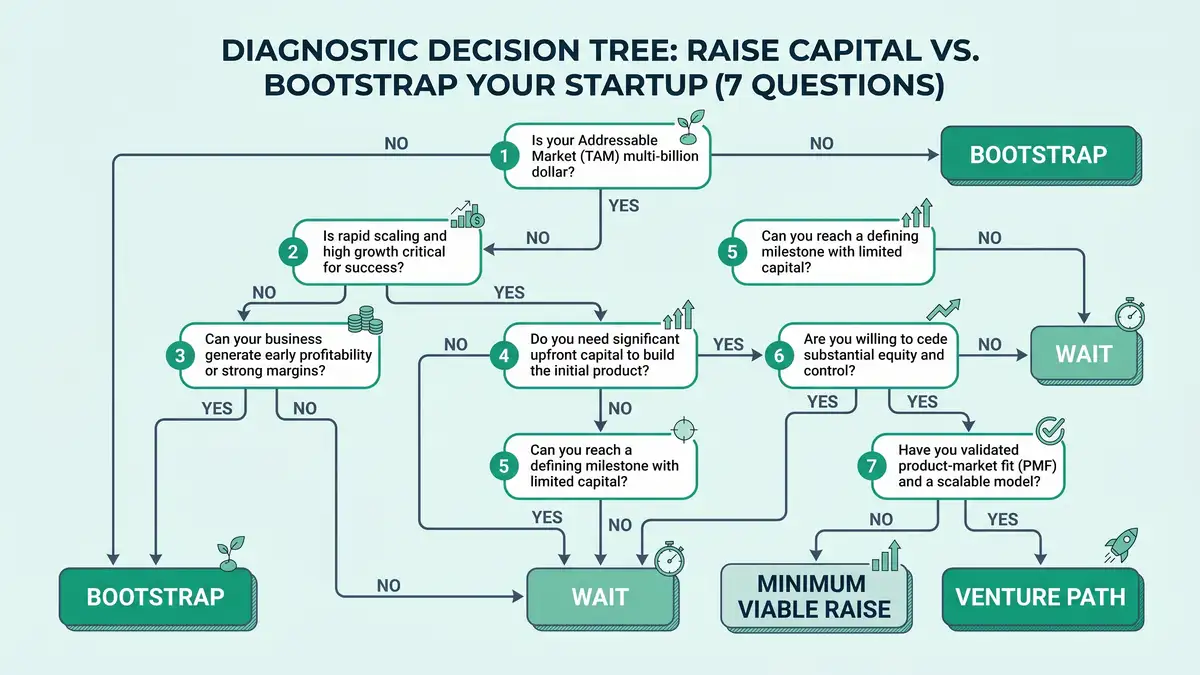

The Seven-Question Decision Framework

Run every founder through this framework. The output is one of four paths: Bootstrap, Minimum Viable Raise, Standard Venture, or Wait. Each question is scored 1-5, and the totals map to the recommended path.

Is the market winner-take-most or fragmented?

Winner-take-most: one or two players capture 60%+ of category revenue (search, social networks, payment networks). Fragmented: top five players each take 10-25% (vertical SaaS, niche tools, agency software). Winner-take-most demands venture; fragmented does not. Score 5 for unambiguous winner-take-most, 1 for unambiguous fragmented.

What is the capital intensity of the GTM motion?

Self-serve PLG and content-led inbound: low capital intensity (sub-$1M to validate). Outbound-heavy enterprise sales: high capital intensity ($5M-$15M minimum to validate the motion). Hybrid PLS sits in the middle. The higher the GTM capital intensity, the stronger the raise signal. See the SaaS GTM strategy framework for the full motion taxonomy.

What is the founder's personal financial runway and risk tolerance?

Founder with 12-24 months of personal runway and high risk tolerance can bootstrap. Founder with under 6 months runway and dependents has a structural reason to raise (a small Seed buys time). This is the most under-discussed variable in the decision and often the binding one.

What is the founder's ownership and control preference?

Founders who want to retain board control, set their own vision, and make M&A or strategic decisions without consulting investors should bias toward bootstrap or minimum-viable-raise. Founders comfortable with investor partnership and external accountability can bias toward standard venture.

What is the growth-rate ambition vs profitability target?

Bootstrap path: 15-25% growth with 25-40% FCF margin, Rule of 40 in the 35-50 range. Venture path: 30-60% growth with negative-to-breakeven FCF, Rule of 40 in the 40-60 range. The two profiles produce different company architectures, so commit to one before scaling. The CEO dashboard tracks both.

What is the exit horizon and outcome range?

Bootstrap exits typically land $20M-$300M, sometimes $1B+ (Mailchimp, Atlassian). Standard venture exits target $500M-$5B+. Heavy venture targets $1B+ unicorn outcomes. If your honest realistic outcome range is $50M-$200M, bootstrap or minimum viable raise produces a better personal outcome.

What are the unit economics today, and are they defensible?

If LTV:CAC sits at 4:1 or higher with sub-15-month CAC payback and gross margin above 80%, the business has the unit-economic profile to grow profitably without venture. If LTV:CAC is below 3:1 or CAC payback is past 24 months, the business is not yet ready for either path; fix product-market fit and motion repeatability first using the GTM motion framework. The SaaS unit economics framework walks through the math, and the CAC benchmark shows where to draw the line.

Want a 90-day capital-strategy diagnostic that maps your unit economics to the right path and sequences the next three quarters of capital deployment?

Book a Freedom Machine DiagnosticHybrid Capital Stacks in 2026

The cleanest decision is rarely binary. Most founders should consider one of three hybrid stacks before defaulting to a Series A.

| Instrument | Use case | Cost | Dilution |

| Venture debt (SVB, JPMorgan, Bridge Bank, Espresso) | Extending runway between equity rounds; fund expansion without dilution | 10-13% interest + warrants 0.5-2% | 0.5-2% (warrant coverage only) |

| Revenue-based financing (Capchase, Pipe, Founderpath, Lighter Capital) | Pull forward 12 months of MRR for marketing or hiring spend at predictable cost | Effective 8-15% per pull | 0% (no equity) |

| Secondary tender | Founder/early-team partial liquidity without primary dilution | Standard secondary discount 10-25% | 0% (no new shares issued) |

| Growth equity (Insight Partners, Vista, Thoma Bravo) | $15M-$50M into already profitable $20M+ ARR SaaS for accelerated expansion | Standard equity | 15-30% per round |

Source: Capchase Non-Dilutive Funding Guide, Carta State of Private Markets 2025-2026.

Six Case Studies: How Real Founders Actually Decided

| Company | Path Chosen | Outcome | Founder Lesson |

| Mailchimp | Pure bootstrap to $700M+ ARR | $12B Intuit acquisition (2021); founders held majority equity | Bootstrap remains viable to mega-outcome scale in fragmented markets |

| Calendly | Bootstrap to $70M ARR, then OpenView $350M Series B | Founder retained majority through bootstrap; raised at $3B valuation | Bootstrap proves the business; raise on your terms once leverage flips |

| Linear | Standard venture (Seed, A, B at $1B+ valuation) | PLG infrastructure category needed brand-and-velocity capital | When the market rewards velocity and design density, venture earns its dilution |

| Basecamp | Bootstrap forever; refused outside capital | Multi-decade profitability; founder optionality preserved | Optionality and control can be the real product |

| Cursor (Anysphere) | Aggressive AI-native venture; $100M+ Series B in 18 months | Reached $100M+ ARR in under 18 months | AI-native winner-take-most categories rebuild the case for venture velocity |

| PostHog | Hybrid: community-led bootstrap, then YC + Series B | $10M+ ARR before raising; raised on community traction | Community-led bootstrap creates the strongest possible Series A leverage |

Source: First Round Review, PostHog Handbook, Bessemer Atlas 2026.

The 30/60/90-Day Implementation Plan

Days 1-30: Financial model and decision confirmation

Build a 36-month financial model with three columns: bootstrap, hybrid, full venture. For each, project revenue, margin, headcount, runway, and founder ownership at 12, 24, 36 months. Run the seven-question framework with scoring. Document the ICP and unit economics required to support your chosen path. Outcome: written decision memo that the leadership team and any co-founder signs.

Days 31-60: Market and competitive position assessment

Validate the market structure assumption (winner-take-most vs fragmented) by mapping the top five competitors with revenue, headcount, and funding history. Assess capital intensity by costing the next $10M of ARR through the GTM motion. Confirm the founder ownership target and validate that the chosen path delivers it. If reality contradicts the Day-30 decision, revise.

Days 61-90: Capital instrument selection and execution

Bootstrap path: tighten unit economics, build cash reserve, line up venture debt or RBF for opportunistic acceleration. Minimum viable raise: target one strategic angel and a small priced Seed (5-10% dilution maximum). Standard venture path: build the data room, line up 25-40 target firms, prepare the 16-slide deck, schedule the first 8 partner meetings. In all cases, the founder controls the timeline rather than reacting to inbound.

Frequently Asked Questions

Should I bootstrap or raise venture capital for my SaaS?

Run the seven-question framework: market structure (winner-take-most or fragmented), GTM capital intensity, founder runway and risk tolerance, ownership and control preference, growth ambition vs profitability target, exit horizon and outcome range, and unit economics defensibility. Bootstrap fits fragmented markets with low GTM capital intensity, founder ownership goals above 50%, exit ranges $50M-$300M, and unit economics with LTV:CAC of 4:1+ already proven. Standard venture fits winner-take-most markets, capital-intensive GTM, $1B+ outcome ambition, and willingness to accept 50-65% dilution by Series C.

How much do founders typically dilute through Seed to Series C?

Standard venture path produces 50-65% founder dilution by the time the company reaches $50M ARR. Seed: 15-25% dilution. Series A: 18-22%. Series B: 15-18%. Series C: 12-15%. Each round also reserves 10-15% for an option pool refresh, which the founder economically funds. By Series C, the original founder typically holds 15-25% of the company. Heavy venture paths (mega rounds, multiple primary issuances) compress this to 5-15% founder ownership. Source: Carta State of Private Markets 2025-2026.

What is the median NRR for bootstrapped SaaS in 2026?

Median NRR for bootstrapped SaaS at $3M-$20M ARR is 103%, with the 90th percentile reaching 117.9%. Bootstrapped SaaS also runs 90%+ gross margins and is typically cash-flow positive at this stage, producing Rule of 40 in the 35-50 range. Source: SaaS Capital 2026 Benchmarking Metrics for Bootstrapped SaaS Companies.

When is venture capital actually required?

Four structural conditions: (1) winner-take-most market dynamics where first-mover scale produces lasting moats; (2) capital-intensive GTM where enterprise sales motion costs $5M-$15M to validate before unit economics work; (3) capital-intensive product where engineering, infrastructure, or hardware capex exceeds $5M before revenue is possible; (4) geographic land-grabs requiring multi-continental simultaneous expansion. Outside these four conditions, venture is optional, not required, and the choice has consequences for ownership, control, and exit pressure.

What are the alternatives to raising venture capital?

Four hybrid instruments fit between pure bootstrap and standard venture: (1) venture debt at 10-13% interest with 0.5-2% warrant coverage, used for runway extension and non-dilutive growth; (2) revenue-based financing from Capchase, Pipe, Founderpath, Lighter Capital, pulling forward 12 months of MRR at 8-15% effective cost with zero dilution; (3) secondary tender offers giving founders and early team partial liquidity at 10-25% discount with zero new dilution; (4) growth equity from Insight, Vista, Thoma Bravo at $20M+ ARR for 15-30% dilution per round. Most $10M-$40M ARR SaaS should consider one of these before defaulting to a Series A.

How long does it take to raise a Series B in 2026?

Median time to close a Series B in 2026 sits at six to nine months from first investor conversation to wired funds, roughly double the 2021 norm. Investors expect $5M+ ARR, 80%+ growth, sub-15-month CAC payback, and Rule of 40 above 40 before serious term sheet conversations begin. AI-native companies absorbed most of the available capital in 2025-2026, leaving traditional SaaS rounds smaller and slower. Founders should plan for 9-12 months of dedicated fundraising effort and ensure 18-month runway before opening the round.

Can a bootstrapped SaaS reach $100M ARR?

Yes. Mailchimp reached $700M+ ARR before its $12B Intuit acquisition in 2021 with founders holding majority equity. Atlassian crossed $1B ARR mostly bootstrapped before its IPO. Calendly reached $70M ARR before raising. Basecamp has run profitably for over two decades without outside capital. The pattern: fragmented markets, strong unit economics from day one, disciplined headcount, and patience over 8-15 year time horizons. The path is harder and slower than venture but produces dramatically better personal outcomes for the founder.

What is revenue-based financing and is it right for SaaS?

Revenue-based financing (RBF) is non-dilutive capital where a SaaS company sells a percentage of future revenue at a fixed multiple. Capchase, Pipe, Founderpath, and Lighter Capital are the primary 2026 providers. Effective cost runs 8-15% per pull, with no equity given up and no board seats. RBF fits SaaS with predictable MRR (90%+ gross retention), $1M+ ARR, and a specific use case (marketing, hiring, expansion) that produces faster-than-cost-of-capital ROI. RBF does not fit pre-PMF companies or those with volatile revenue.

Capital strategy is company architecture. Architect it like one.

peppereffect installs the unit-economics model, the seven-question diagnostic, the hybrid capital stack, and the operating cadence that takes a $5M to $40M ARR SaaS through the right capital path for the founder's actual goal. The result: ownership preserved where it should be, capital deployed where it earns its dilution, and a board you actually want. board reporting template

Architect Your Freedom MachineResources

- SaaS Capital: 2026 Benchmarking Metrics for Bootstrapped SaaS Companies

- Bessemer Atlas: State of the Cloud 2026

- High Alpha: SaaS Fundraising in 2026: What Data Tells Us

- Carta: State of Private Markets 2025-2026

- Index Ventures: Founder Sharing Survey

- Capchase: A B2B SaaS Founder's Guide to Non-Dilutive Funding

- IdeaProof: Bootstrap vs VC Funding 2026 Comparison

- Capidel: Bootstrap vs Raise Capital 2026 Founder Funding Decision

- First Round Review: Going from PLG to Enterprise

- PostHog Handbook: No Outbound (Hybrid Bootstrap-then-Raise)