Rule of 40: The SaaS Metric That Balances Growth and Profitability

If you run a B2B SaaS company between $10M and $40M ARR, your board has asked one version of this question in your last three meetings: can we keep growing fast and start making money at the same time? The Rule of 40 is the metric they are using to decide. Sum your annual ARR growth rate and your profit margin — the answer should be 40 or higher. That single number now correlates more tightly with your valuation, your acquisition multiple, and your fundraising room than any other operational metric on the dashboard.

The reason it matters in 2026 is brutal arithmetic. ICONIQ's 2025 State of Software report identifies the Rule of 40 as the single most reliable predictor of valuation across the cloud software universe. Bessemer Venture Partners publicly shifted to a free-cash-flow-margin variant in early 2024 because adjusted-EBITDA gymnastics had stopped fooling buyers. Meanwhile, ICONIQ's same dataset shows AI-native SaaS companies growing two-to-three times faster than the top-quartile benchmark, often while expanding margin — proving the Rule is achievable at mid-market scale, but only with a different operating system.

This guide is the operator's playbook: definition, formula, the six levers that actually move the score, where mid-market SaaS gets stuck, and how agentic AI architecture is rewriting the math for $10M–$40M ARR companies. We've installed the Rule of 40 architecture for B2B SaaS founders and the patterns repeat. Use this as a working blueprint, not a textbook.

Bottom Line Up Front

For a $10M–$40M ARR B2B SaaS, the Rule of 40 is the most defensible single signal of capital efficiency for boards, VCs, and acquirers. Only 15–20% of mid-market SaaS hit it because the math punishes companies stuck between growth-stage burn and scale-stage leverage. The fastest path through that valley is not cost-cutting — it's compressing CAC and lifting revenue per employee through agentic AI workflows, then locking in margin via NRR >120% and disciplined pricing. Companies that crack this combination earn a 2.5–3× valuation premium against their below-40 peers.

Want to see your own CAC against peer benchmarks? Run the CAC Diagnostic for your true CAC, the 30 to 50% reduction agentic deployment delivers, and a board-ready PDF in 60 seconds.

Run the CAC DiagnosticWhat Is the Rule of 40?

The Rule of 40 originated with venture capitalist Brad Feld's 2015 observation that the SaaS companies in his portfolio that compounded reliably over time consistently scored at least 40 when you summed their year-over-year revenue growth rate and their EBITDA margin. The formula is intentionally simple:

Rule of 40 Score = ARR Growth Rate (%) + Profit Margin (%) ≥ 40

The reason 40 is the threshold is empirical, not theoretical. Feld observed it across 100+ portfolio companies — at scale, businesses that consistently hit 40 sustained value creation through cycles, while businesses below 40 either burned through cash chasing unprofitable growth or stagnated in low-growth profitability. Wall Street Prep's Rule of 40 reference documents the original framing and the math is unchanged a decade later.

What has changed is which margin you put on the right side of the equation. The classic formulation used EBITDA margin. By 2024, sophisticated public-market analysts and PE buyers had migrated to a Free Cash Flow margin variant, and Bessemer publicly endorsed the shift. The reason is straightforward: stock-based compensation can represent 20–35% of operating costs at growth-stage SaaS, and adjusted-EBITDA reporting that adds it back inflates apparent profitability while burning real cash. FCF margin closes that gap.

For Sarah Chen's cohort — mid-market B2B SaaS CEOs running between $10M and $40M ARR — the operating answer is to report Rule of 40 using ARR Growth + FCF Margin. It is more defensible to your board, more credible to acquirers, and signals financial discipline that growth-only narratives can no longer carry post-2022.

The Three Variants You'll See in 2026 Reporting

| Variant | Formula | When to Use | 2026 Credibility |

| Classic (EBITDA) | ARR Growth % + EBITDA Margin % | Legacy reporting; older board decks | Declining — flagged for stock-comp manipulation |

| FCF Margin (preferred) | ARR Growth % + FCF Margin % | Public analysts, sophisticated PE, M&A buyers | 2026 standard — cash-based, manipulation-resistant |

| Operating Income Margin | ARR Growth % + Operating Margin % | Middle ground; some boards | Acceptable; less common than FCF |

Source: Bessemer / Fortune (2024), Cambria Private Capital — Rethinking the Rule of 40 (2024).

Want to know exactly which of these levers would reclaim the most hours in your business? Take the 4-minute Technician's Trap Scorecard.

Get My Personalised ReportHow to Calculate the Rule of 40 (Worked Example)

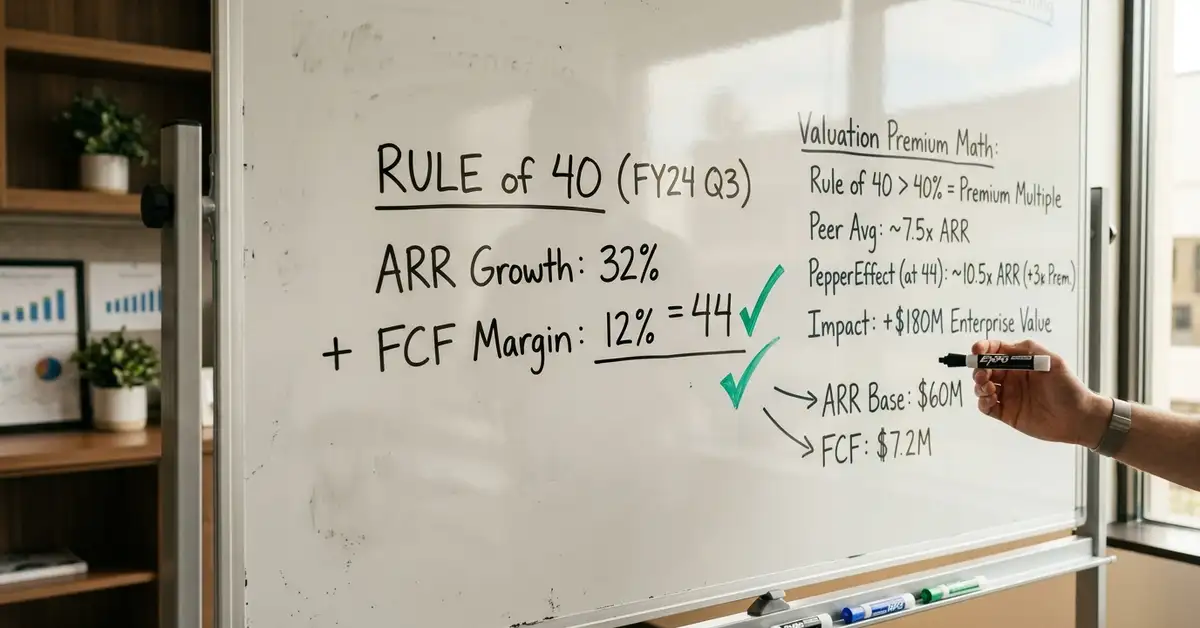

Take a hypothetical mid-market B2B SaaS at $30M ARR growing 32% year over year, with $3.6M in free cash flow on $30M revenue (12% FCF margin):

Calculate ARR Growth Rate

(Current ARR − Prior ARR) ÷ Prior ARR × 100. From $22.7M to $30M = 32.2% ARR growth. Use ARR, not total revenue — services and one-time fees inflate the numerator and undermine the signal.

Calculate FCF Margin

(Operating Cash Flow − CapEx) ÷ Revenue × 100. $3.6M FCF on $30M revenue = 12.0% FCF margin. Use last twelve months (LTM) — single quarters are seasonally distorted and won't survive due diligence.

Sum and Compare

32.2% + 12.0% = 44.2 — Rule of 40 achieved with a 4-point cushion. A 4-point buffer matters: it absorbs a quarter of softness without breaching the threshold and triggering board questions or multiple compression.

Decompose the Quality of the Score

Sophisticated buyers won't accept the headline number alone. They want the breakdown: how much of the 32% growth came from net revenue retention versus net new logos versus acquired contribution? A 32% ARR growth at 125% NRR is materially higher quality than 32% growth at 95% NRR. Always report the decomposition alongside the score.

Source: The SaaS CFO — Rule of 40 calculation guide, Breaking into Wall Street — Rule of 40 with Excel examples.

Why Rule of 40 Drives Your Valuation Multiple

The Rule of 40 is not a vanity metric. It maps almost cleanly to the EV/ARR multiple your business will trade at — whether you are pricing a Series C, negotiating a strategic acquisition, or running a board valuation review. ICONIQ's 2025 State of Software report identifies it as the most reliable single predictor of valuation across the cloud universe — outperforming standalone growth rate or standalone margin.

| Rule of 40 Score | EV/ARR Multiple (Median, 2024–25) | vs. 2021 Peak |

| >50 (Elite) | 8–12× | ~−35% (was 12–18×) |

| 40–50 (Healthy) | 6–9× | ~−45% (was 11–15×) |

| 30–40 (Marginal) | 3–6× | ~−50% (was 6–10×) |

| <30 (Underperforming) | 2–4× | ~−60% (was 5–8×) |

Source: ICONIQ State of Software 2025, Rule of 40 valuation premium analysis.

The 2026 multiple environment compresses everything 40–60% below 2021 peak — but the relative premium for hitting 40 is intact. A Rule of 40 company commands roughly 2.5–3× the EV/ARR multiple of a sub-30 peer. On a $30M ARR business, that is the difference between an 8× exit ($240M) and a 3× exit ($90M). Same revenue, same product, $150M of valuation deltas decided by one operating metric.

This is why we install Rule of 40 architecture as a deliberate operating system, not a back-of-envelope check. The score is a leading indicator of every funding round and exit conversation a CEO will run between $10M and $100M ARR.

Why Mid-Market SaaS Struggles to Hit 40

If you run a $10M–$40M ARR SaaS, your peers face the same brutal math. ICONIQ's Compass software benchmarks show this cohort typically grows 35–55% YoY and operates at FCF margins between −10% and +8%. That gives a typical Rule of 40 score in the high 30s — close, but consistently below the threshold. SaaS Capital's private SaaS dataset reaches the same conclusion: only 15–20% of $10–$50M ARR companies achieve Rule of 40 in any given year.

The structural reasons are three:

Sales and marketing intensity stays high. To sustain 35–50% growth you typically spend 35–50% of revenue on S&M. That intensity does not relax until you cross roughly $50M ARR, which is also where sales efficiency leverage starts to dominate. Until then, every incremental dollar of growth costs you margin. This is the same mechanic we cover in detail in our customer acquisition cost and LTV to CAC ratio guides.

R&D lock-in suppresses operating leverage. Growth-stage SaaS invests 20–35% of revenue in R&D. That ratio rarely drops below 15% before you cross $100M ARR. Until it does, revenue growth can't translate cleanly into margin expansion.

Headcount scales with revenue, not faster. Revenue per employee at the $10–$40M ARR cohort sits at $150k–$250k per FTE. The Rule of 40 cohort average sits at $200k–$300k per FTE — 20–30% above the median. AI-native operators are now hitting $300k–$400k per FTE, a tier we explored in our revenue per employee benchmarks guide. Without that productivity differential, you are scaling headcount roughly in line with revenue, which keeps margin trapped.

The implication: hitting Rule of 40 at $10–$40M ARR is not a rounding-error achievement. It places a company in the top 15–20% of its cohort. That is a credible signal to a board contemplating a Series C, a strategic acquirer running comps, or a PE buyer modeling LTV.

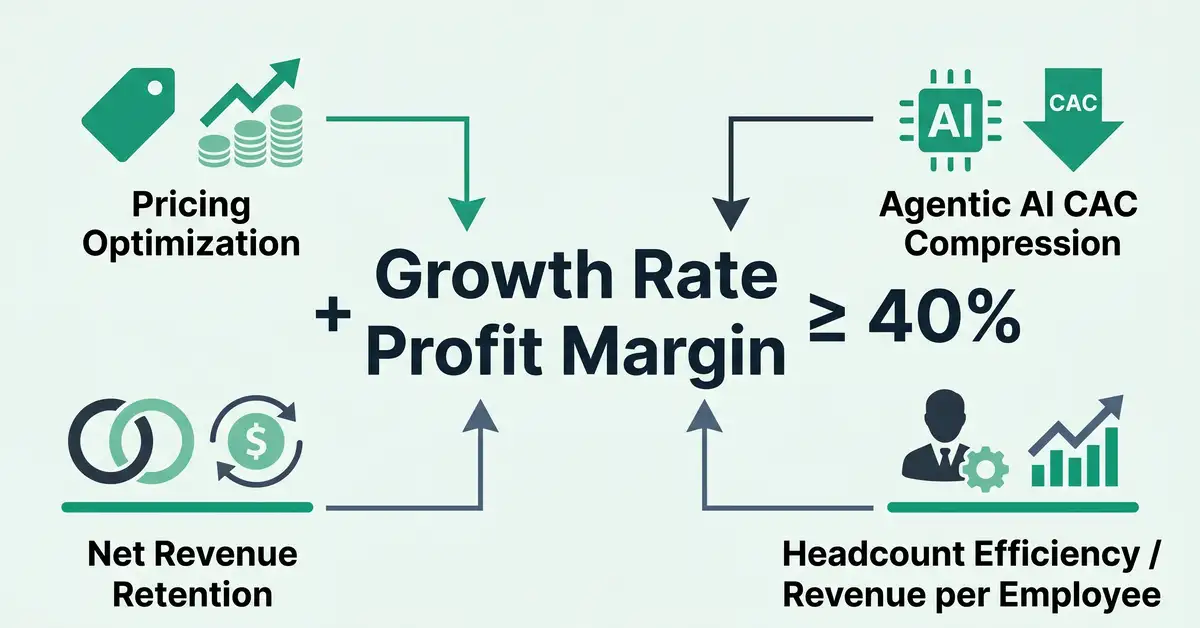

The Six Levers That Actually Move the Score

The arithmetic of the Rule of 40 is unforgiving but the levers are well understood. Six of them, in priority order for a mid-market B2B SaaS operator:

| Lever | Mechanism | Typical Impact |

| 1. Pricing Optimization | 10–15% annual price increases against value releases | +1 to +3 margin points |

| 2. NRR / Expansion Revenue | Drive net revenue retention >120% via upsell, cross-sell, usage | +3 to +6 margin points (high-quality) |

| 3. Agentic AI CAC Compression | Autonomous SDR + agentic qualification + automated nurture | +2 to +4 margin points (15–25% CAC reduction) |

| 4. Revenue per Employee Lift | Headcount efficiency via agentic AI in sales, CS, finance ops | +1 to +2 margin points (10–15% productivity gain) |

| 5. COGS Reduction | Infra optimization, vendor consolidation, model compression | +1 to +3 margin points |

| 6. Magic Number Improvement | Faster sales cycles, higher contract values, lower churn | +2 to +5 margin points |

Source: ICONIQ Compass Software Benchmarks, McKinsey — SaaS and the Rule of 40.

The first two levers are mechanical: every operator should be running them. The third and fourth are where peppereffect's positioning actually moves the needle for mid-market SaaS — and where most competitors stop short. Let's take them one at a time.

Lever 1: Pricing Optimization

A 10–15% annual price increase paired with value releases (new features, tier upgrades, packaging changes) typically drives 0–3% incremental churn and flows roughly 90% to gross margin. On a $30M ARR base, a clean 10% price lift adds $3M of recurring revenue at near-zero incremental cost — that's 1–2 percentage points of margin in a single move. The trick is sequencing: random price hikes generate churn spikes; price increases tied to product value land. We unpack this in detail in our B2B pricing strategy guide.

Lever 2: NRR / Expansion Revenue (the highest-quality growth)

NRR-driven growth is 3–4× higher margin than new-logo growth because it carries no incremental CAC. Top-quartile SaaS hits 125–145% NRR; the Rule of 40 cohort averages 110–120%; below-40 peers average 95–105%. The leverage: a company running 130% NRR can hit Rule of 40 at 25–30% ARR growth instead of needing 40%+. Our expansion revenue strategy and customer success automation guides cover the playbook.

Lever 3: Agentic AI CAC Compression — Peppereffect's Core Thesis

This is where mid-market SaaS gets unblocked. McKinsey's SaaS and the Rule of 40 research documents that AI productivity gains of 10–15% are reshaping the underlying economics. Operators deploying autonomous SDRs, agentic qualification, and automated nurture are reporting 15–25% CAC reduction within 6–12 months. On a $30M ARR base spending $7.5M on S&M, a 20% CAC compression frees roughly $1.5M of margin — directly lifting Rule of 40 by 2–4 points.

The mechanism is structural, not incremental. Agentic workflows replace human-bound process steps with autonomous agents that run 24/7, qualify against rich context, and route at machine speed. Our B2B sales automation and AI for SaaS playbooks document the architecture; the Rule of 40 score is the downstream proof.

Lever 4: Revenue per Employee Lift via Agentic AI

McKinsey's analysis on Rule of 40 leaders highlights that the highest-performing operators set growth targets based on what is organically achievable inside their current cost base — they don't bolt on headcount to chase outsized numbers. Translating that into 2026 reality: deploying agentic AI in sales operations, customer success, and finance/planning typically yields 10–15% headcount efficiency, which translates to 1–2 margin points without sacrificing capacity. It's why our capacity expansion playbook centers on AI-native operators rather than headcount scaling.

Levers 5 and 6: COGS Discipline and Magic Number

COGS reduction (cloud-cost optimization, vendor consolidation, AI model compression) typically yields 1–3 margin points but compounds well alongside the other levers. Magic Number — net new ARR divided by S&M spend — is your single best operational read on whether the other five levers are working. Rule of 40 companies average a Magic Number of 0.8–1.2; below-40 peers average 0.4–0.7. We dig into the operating model in our SaaS unit economics guide.

Architect your Rule of 40 path with a Growth Mapping Call

Get a structural read on which levers are actually closing for your $10M–$40M ARR business — and which agentic AI workflows compress CAC and lift RPE fastest in your specific category. We don't speculate. We diagnose, then install.

Book your Growth Mapping CallFive Mistakes That Kill the Rule of 40 Signal

1. Manipulating EBITDA via stock-comp add-backs. Stock-based compensation can be 20–35% of operating costs at growth-stage SaaS. Adjusted-EBITDA reporting that adds it all back inflates apparent profitability while burning real cash. Bessemer's 2024 shift to FCF margin signaled that institutional investors no longer accept this as a defensible metric. Use FCF margin in board reports.

2. Comparing Rule of 40 across stages. A $10M ARR company hitting 40 is doing something materially harder than a $200M ARR company hitting 40. SaaS Capital's private SaaS data shows the cohort distributions explicitly: ~15–20% of $10–$50M ARR companies hit it, ~30–40% of $50–$100M ARR companies, ~40–50% of $100M+ ARR. Apply stage-adjusted context.

3. Ignoring quality of growth. A 40% ARR growth from net new logos is not the same as 40% growth from 130% NRR. Sophisticated buyers decompose the score into organic growth, inorganic (M&A) contribution, and one-time/services revenue. Lead with the decomposition in board decks; don't make them ask.

4. Reporting single-quarter Rule of 40. Quarterly numbers are seasonally distorted and won't survive due diligence. Ordway Labs' SaaS metrics framework reinforces that LTM/TTM Rule of 40 is the standard institutional view. Report on a trailing 12-month basis, every time.

5. Treating Rule of 40 as the ceiling. The frontier has moved. Industry analysts now reference Rule of 50 (and Rule of 60 for elite operators) as the AI-era differentiator. Top-quartile public SaaS is converging on Rule of 50 with 25–35% ARR growth and 20–35% FCF margins. Plan your scoring trajectory accordingly.

How Agentic AI Changes the 2026 Math

The Rule of 40 wasn't designed for a world where customer acquisition cost can drop 25% in a year and revenue per employee can rise 15% in the same span. ICONIQ's 2025 State of Software data on AI-native SaaS shows these operators growing 2–3× faster than traditional top-quartile benchmarks, while expanding margin — a combination the original 2015 framework didn't anticipate.

The practical implication for a $10M–$40M ARR CEO is that the path to Rule of 40 has shortened. Pre-2024, getting from a Rule of 35 to a Rule of 40 typically took 18–24 months of disciplined sales-efficiency work. With agentic workflows in place, we see the same swing happening in 8–12 months because two levers (CAC compression and RPE lift) move simultaneously rather than sequentially. The infographic above maps the four highest-leverage levers; we install all four as one operating system, not four separate projects.

The same data implies a sharper warning. As more operators install AI-native architecture, Rule of 40 becomes table-stakes. The differentiation in 2027 valuations will sit at Rule of 50. The window for outperformance is now.

Frequently Asked Questions

What is the Rule of 40 in SaaS?

The Rule of 40 is a SaaS performance benchmark holding that a company's annual ARR growth rate plus its profit margin should sum to at least 40. Originated by Brad Feld in 2015 from VC portfolio observation, it has become the most reliable single predictor of SaaS valuation, with companies above 40 typically commanding 2.5–3× the EV/ARR multiple of below-40 peers.

How do you calculate the Rule of 40?

Add your annual ARR growth rate to your profit margin — both expressed as percentages — and check whether the sum is 40 or higher. The 2026 standard uses ARR growth plus FCF margin (rather than EBITDA margin) on a trailing twelve-month (LTM) basis. For example, 32% ARR growth plus 12% FCF margin equals 44, achieving Rule of 40 with a 4-point cushion.

What is a good Rule of 40 score for a SaaS company?

Any score of 40 or higher is considered healthy, with each tier signaling progressively stronger value creation. The 2026 distribution shows roughly 30% of public SaaS hitting Rule of 40, only 15–20% of $10M–$50M ARR private SaaS, and an emerging top-quartile cohort hitting Rule of 50 or higher. For mid-market B2B SaaS, achieving 40 places you in the top fifth of your cohort and is a meaningful board, fundraising, and acquisition signal.

Should I use EBITDA margin or FCF margin for the Rule of 40?

FCF margin. Adjusted-EBITDA reporting can inflate apparent profitability by adding back stock-based compensation, which represents 20–35% of operating costs at growth-stage SaaS and burns real cash. Bessemer Venture Partners publicly shifted to FCF margin in 2024, and sophisticated public-market analysts and PE buyers now treat FCF margin as the institutional default. Reporting Rule of 40 via FCF margin signals discipline and is more defensible in due diligence.

Why is the Rule of 40 hard to achieve at $10M–$40M ARR?

Three structural reasons. Sales and marketing intensity has to stay at 35–50% of revenue to sustain growth. R&D investment is locked at 20–35% of revenue. And headcount scales roughly in line with revenue because operating leverage doesn't compound below approximately $50M ARR. Together these forces typically produce FCF margins between −10% and +8%, leaving Rule of 40 just out of reach unless agentic AI compresses CAC and lifts RPE fast enough to break the trade-off.

How do I improve my Rule of 40 score?

Six levers, in priority order: 1) annual price increases of 10–15% paired with value releases; 2) drive net revenue retention above 120% via expansion revenue; 3) compress CAC 15–25% via agentic AI workflows in sales and qualification; 4) lift revenue per employee 10–15% through AI-native operations across sales, CS, and finance; 5) reduce COGS via cloud and vendor optimization; 6) improve Magic Number above 1.0× by shortening sales cycles and lifting contract values. Companies installing all six as a single operating system typically swing from Rule of 35 to Rule of 40 in 8–12 months.

Resources

- McKinsey — SaaS and the Rule of 40: Keys to the critical value creation metric

- ICONIQ Capital — State of Software 2025: Rethinking the Playbook

- ICONIQ Compass — Software Benchmarks Dashboard

- Fortune — Bessemer Venture Partners Rule of 40 valuation shift (2024)

- SaaS Capital — Growth, Profitability, and the Rule of 40 for Private SaaS

- Cambria Private Capital — Rethinking the Rule of 40: Bessemer's Growth-Weighted Approach

- Wall Street Prep — Rule of 40 (Brad Feld) Formula and Calculator

- The SaaS CFO — Rule of 40 SaaS calculation guide

- Breaking Into Wall Street — Rule of 40 with Excel examples

- Ordway Labs — Rule of 40 formula, benchmarks, and when it matters

- SaaS Metrics Standard Board — Rule of 40 Reference

- Driven Insights — How to Use the SaaS Rule of 40 Playbook

- Compound with Rene — Reinvention of the Rule of 40 (Rule of X)

- Paylocity — Rule of 40 glossary reference

- Next Big Teng — Rule of 40 valuation premium analysis

The Rule of 40 is the single highest-leverage operating signal a mid-market B2B SaaS CEO has. It is also the metric most often reported badly. Get the formula right (FCF margin, LTM basis), decompose growth quality, install the six levers as one operating system, and the score becomes a board, fundraising, and acquisition asset rather than a quarterly inquisition.

If your $10M–$40M ARR business is sitting at Rule of 35 and you want to architect the swing to Rule of 40 — or beyond, into the AI-native Rule of 50 frontier — let's diagnose where the leverage actually sits and install the architecture. Book a Growth Mapping Call and we'll map the path against your specific cost base, sales motion, and product velocity. capital efficiency operating system 12-metric Monday dashboard SaaS board deck template