The recruitment firm valuation question is the one every founder asks at some point: what is the business actually worth, and what would it take to maximise that number? The answer is structural rather than sentimental. Recruitment firms trade on EBITDA multiples calibrated to a defined set of value drivers, and the gap between a 3x and a 12x multiple on the same revenue base is the difference between a respectable exit and a generational outcome.

This article installs the valuation framework that boutique to mid-market executive search firms (5-50 consultants, $5-50M revenue) use to understand current worth, identify the value drivers that compound multiples, and prepare for exit, succession, or capital raise. James Sterling, Managing Director of a global executive search boutique, will use this as the strategic asset that decouples retirement timing from a single market window.

The valuation thesis

Recruitment firms do not trade on revenue, headcount, or founder reputation. They trade on adjusted EBITDA multiplied by a multiple calibrated to seven specific value drivers and discounted by seven specific destroyers. The boutique founder who understands the multiple math and runs the firm to maximise the drivers achieves 2-3x the exit value of an equivalent founder operating on intuition. The 24-36 month preparation window before market is the highest-leverage strategic discipline in the firm's lifetime.

The fundamentals: how recruitment firms are valued

Recruitment firms trade primarily on adjusted EBITDA multiples. For owner-operator firms below $5M revenue, the alternative metric is Seller's Discretionary Earnings (SDE) which adds back owner compensation, owner benefits, and one-time items. For firms above $5M revenue with a functional management team, EBITDA is the standard. ClearlyAcquired's analysis of EBITDA versus SDE methodology documents the threshold where each metric applies. The fee structure that produces these EBITDA characteristics is covered in executive search pricing models.

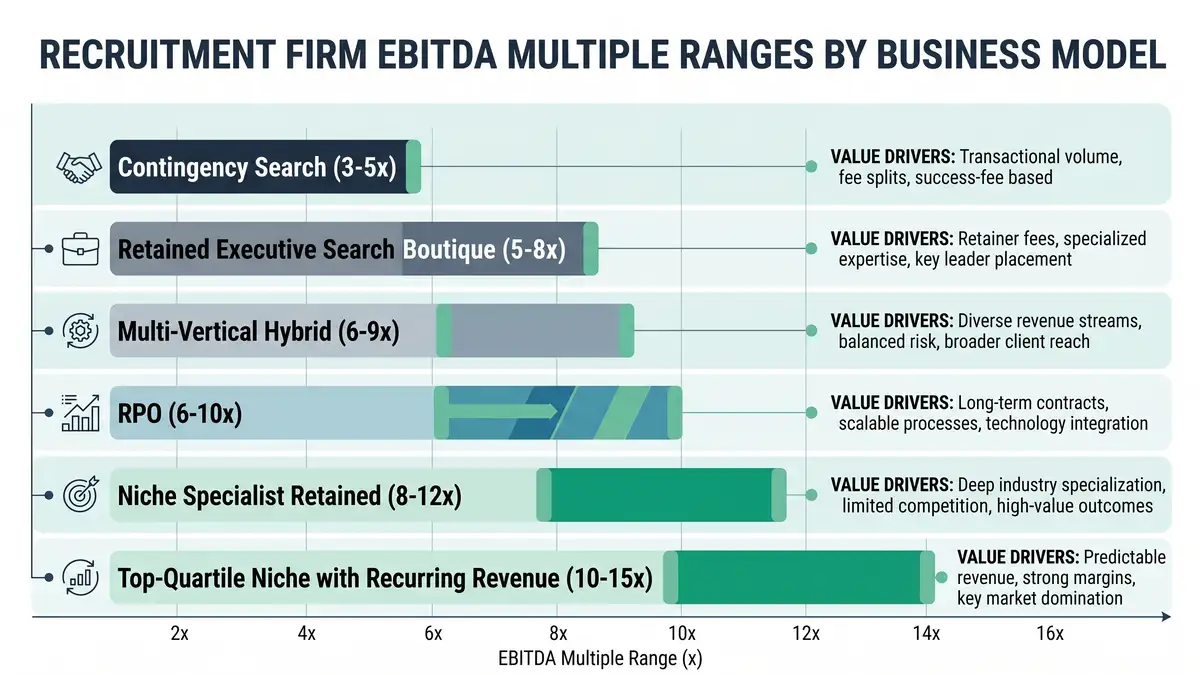

The EBITDA multiple ranges differ sharply by firm model. Equidam's EBITDA multiples by industry analysis places general staffing in the 3-6x range. Multiples.vc recruitment and staffing valuation multiples and ValuAnalytics recruiting and staffing valuations confirm the dispersion. Top-quartile niche specialist retained search firms with recurring advisory revenue command 10-15x or more. The 5x spread between an undifferentiated generalist and a defensible niche specialist on identical EBITDA is the structural insight that drives the value-driver framework. See niche vs generalist recruitment for the strategic positioning matrix that determines which multiple band the firm occupies.

| Firm model | Typical EBITDA multiple | Driver characteristics |

| Contingency search (general) | 3-5x | Transactional, low repeat, high consultant turnover |

| Retained executive search boutique (generalist) | 5-8x | Higher fees, mid-tier repeat, founder-dependent |

| Multi-vertical hybrid with practice areas | 6-9x | Diversified, scale economics, practice-area depth |

| RPO (recurring contract revenue) | 6-10x | Recurring revenue, contract length, multi-year visibility |

| Niche specialist retained search | 8-12x | Sector authority, premium fees, deep talent pool |

| Top-quartile niche with advisory revenue | 10-15x+ | Recurring advisory, multi-product, low founder dependency |

Sources: FirstPageSage EBITDA multiples by industry, Equidam EBITDA multiples, ValuAnalytics recruiting and staffing valuations 2024, Multiples.vc recruitment valuation.

The mathematics is brutal. A $20M revenue firm at 25% EBITDA margins generates $5M EBITDA. At 4x (undifferentiated contingency) that values at $20M. At 10x (niche specialist) the same firm values at $50M. The same operational performance, the same client base, the same consultants, but a 2.5x difference in exit proceeds determined entirely by where the firm sits on the multiple curve. See recruitment firm profitability for the margin mechanics that combine with multiples to produce enterprise value.

The 7 value drivers that compound multiples

Seven structural characteristics determine where in the multiple range a firm lands. Each driver scores 1-5 in the typical M&A advisor evaluation. RPO Media analysis of valuation benchmarks for niche recruiting firms documents the standard buyer scorecard. Hunt Scanlon's analysis of market shift and founder-led exits confirms which drivers buyers weight most heavily in current market conditions.

| Value driver | Premium signal | Multiple impact |

| 1. Revenue concentration | Top 5 clients less than 40% of revenue | +1-2x premium |

| 2. Repeat client share | 60-75% revenue from repeat clients | +1-2x premium |

| 3. Recurring revenue | RPO contracts, retained advisory, talent intelligence subscriptions | +2-3x premium |

| 4. Consultant retention and bench depth | 82%+ annual retention, 2+ partners ready to step up | +1-2x premium |

| 5. Sector authority and niche position | Documented thought leadership, top-3 sector ranking | +2-4x premium |

| 6. Operating system documentation | Written operations manual, CRM discipline, governance cadence | +0.5-1x premium |

| 7. Founder dependency | Founder generates less than 40% of mandates | +1-2x premium |

Sources: Recruiter Insider on boosting valuation before sale, CorpInvest on factors that turn 3x into 5x, Talant Staffing on maximising staffing firm valuation.

The cumulative effect compounds. A boutique scoring 5/5 on all seven drivers commands the top of the multiple range. A boutique scoring 2/5 on average sits at the bottom regardless of EBITDA size. See managing client relationships in executive search for the partnership model that drives revenue concentration improvement, and recruitment firm operations manual for the documented operating system that drives the governance premium.

The 7 value destroyers that compress multiples

1. Single client greater than 25% of revenue

Customer concentration is the single most common reason boutique firms receive multiple discounts. Buyers apply 15-30% valuation haircuts when one client exceeds the 25% threshold, regardless of relationship depth. Morgan and Westfield analysis of concentration risk documents the buyer math.

2. Founder generates greater than 70% of BD

The founder-dependent firm is the founder's job, not a transferable business. SE Advisory analysis of founder dependency as hidden valuation killer shows the 30-50% multiple discount buyers apply when founder departure would destroy more than half of pipeline. Brentwood Growth on owner involvement and valuation outlines remediation.

3. Consultant churn greater than 25% annually

High consultant turnover signals broken operating culture, weak performance management, or unsustainable economics. Buyers apply 10-20% multiple discount because the post-acquisition retention risk is acute. Elite firms maintain 82%+ retention through structured onboarding, clear performance management, and competitive compensation.

4. No documented operating system

The firm that operates on tribal knowledge has no asset to transfer beyond the people. Documentation gaps translate directly to multiple compression because acquirers see deal risk in every undocumented process.

5. Concentration in one cyclical sector

Pure FinTech, pure crypto, pure enterprise SaaS specialists trade at higher multiples in upcycles and absorb proportional discounts in downcycles. BCG analysis of cyclical sector navigation covers the diversification economics. Pair the dominant niche with 1-2 counter-cyclical adjacent verticals.

6. Inconsistent EBITDA history

Buyers value 3-year trailing EBITDA with smoothing for outliers. A firm with $2M, $8M, $3M EBITDA over 3 years values lower than $4.3M average suggests because the inconsistency signals revenue volatility. Windes on EBITDA normalisation details the smoothing methodology.

7. Earnings tied to non-recurring large mandates

A single $2M placement fee distorts the trailing 12 months EBITDA upward but adds no value to enterprise multiple because buyers exclude non-recurring revenue. Rob Go analysis of non-recurring revenue businesses details how non-recurring revenue receives lower multiples than the headline EBITDA suggests.

The quality-of-earnings process

Every serious M&A transaction runs a quality-of-earnings (QoE) analysis before final pricing. The QoE adjusts reported EBITDA to reflect the true ongoing earning power of the business. Warren Averett's quality-of-earnings methodology documents the standard adjustments. Wall Street Prep on normalised EBITDA shows the technical mechanics.

The QoE workflow runs four phases. Phase one normalises owner compensation to market rate (replacing $500k owner draw with $250k market salary increases reported EBITDA by $250k). Phase two strips one-time items (legal settlements, asset sales, COVID grants, restructuring costs). Phase three removes related-party transactions priced off-market (founder personal expenses run through the business, intercompany charges). Phase four reviews working capital normalisation and capex projections for the buyer's pro forma model.

Customer concentration tests, consultant retention analysis, and revenue recurrence assessments run alongside the EBITDA work. The QoE report typically takes 6-10 weeks and costs $50k-$200k depending on firm size. The investment pays back through credibility with sophisticated buyers and through the QoE process itself surfacing value driver gaps that founders can address pre-transaction.

The 4 buyer types and what each pays

Different buyer categories pay different multiples for the same firm. Understanding the buyer landscape is essential to maximising exit value. Auxo Capital Advisors on why strategic buyers pay more documents the synergy premium.

| Buyer type | Typical multiple range | Deal characteristics |

| Strategic acquirer (large search firm) | 8-12x | Synergy premium for true sector authority; integration risk |

| Private equity platform investment | 6-10x | Buy-and-build thesis; new platform creation |

| PE add-on to existing platform | 5-8x | Bolt-on to existing portfolio; cost synergy focus |

| Management buyout | 4-7x | Seller financing common; longer payment structure |

Sources: Lion Business Brokers on PE consolidators buying staffing firms, Dars Law on management buyout exit strategy.

Recent transactions document the pattern. Russell Reynolds' acquisition of tech executive search firm Savage Partners shows the strategic acquirer pattern paying for sector niche authority. CSI Companies' acquisition of MedSys Group illustrates the platform expansion strategy where the acquirer pays for healthcare IT sector entry.

Industry M&A activity 2025-2026

The recruitment M&A market accelerated through 2025 with double-digit growth forecast for 2026. Hunt Scanlon's analysis of recruitment M&A surge in 2025 documents the deal volume rebound from the 2023-2024 trough. Bullhorn GRID 2026 industry trends report confirms that 56% of firms reported revenue growth in 2025, providing the cash flow visibility that supports premium acquisition multiples.

Private equity consolidator activity dominates the deal flow at the boutique scale. Lion Business Brokers' analysis of PE consolidators buying staffing firms documents the buy-and-build thesis driving the market. Strategic acquirers like AMS, RGF Staffing, Korn Ferry, and Russell Reynolds continue to acquire niche specialists where the sector authority complements the existing portfolio.

The boutique segment growing 12-18% annually means more $5-20M revenue firms qualify for institutional buyer attention than at any point in the prior decade. The implication for James Sterling: the optimal exit window is 24-36 months from now, which means starting the value driver optimisation work immediately.

Preparation timeline: 24-36 months to maximum value

The firm that goes to market without preparation typically achieves 60-70% of its maximum achievable value. The 24-36 month preparation window splits into three strategic phases.

Phase one (months 1-12) focuses on de-risking. Eliminate the founder bottleneck by hiring or promoting BD specialist coverage that takes founder personal mandate share below 50%. Reduce single-client concentration below 20% through aggressive new client acquisition in the dominant niche. Document the operations manual and embed it in CRM workflows. See scaling a recruitment firm for the de-risking sequence.

Phase two (months 13-24) focuses on growth acceleration. Install the AI augmentation layer that compounds productivity, including the integrated recruitment technology stack that institutional buyers underwrite as a value driver. Build the recurring revenue base through RPO contracts or retained advisory engagements. Drive the EBITDA trajectory toward the upper end of the multiple band through margin expansion. See executive search business development for the BD operating system that fuels growth.

Phase three (months 25-36) focuses on market preparation. Engage M&A advisor 12 months pre-market. Complete quality-of-earnings preparation 6-9 months pre-market. Map the named buyer landscape with concrete deal precedents. Develop the management presentation that articulates the equity story buyers need to underwrite the premium multiple.

Need to architect the value driver optimisation that compounds your firm's exit multiple?

Industry benchmarks: where elite firms sit

Elite boutiques operate to specific operational benchmarks that translate directly into premium multiples. Hunt Scanlon's Top 50 Americas ranking documents the operational characteristics of the firms commanding the highest multiples. Revenue per consultant in elite firms reaches $800k-$1.5M versus $400k-$700k for average boutiques. EBITDA margins for top-quartile niche specialists reach 30-35% versus 15-20% for unfocused generalists. Time-to-shortlist sits at 2-6 weeks versus 8-12 weeks for the industry average.

The 2026 industry growth rate of 11% per Hunt Scanlon's recruitment M&A surge analysis means the firms that grew faster than 25% over the trailing 12 months attract significant premium multiples because buyers underwrite continued outperformance. The 8% growth firm trades at industry-average multiples; the 30% growth firm trades at premium multiples even before the value driver scorecard.

8 common pitfalls in recruitment firm valuation

1. Relying on revenue multiples for boutiques

Revenue multiples (typically 0.5-1.5x annual revenue) understate the value of high-margin niche specialists and overstate the value of low-margin contingency firms. EBITDA multiples are the correct valuation method above $5M revenue.

2. Ignoring customer concentration risk

The founder convinced that the 35% client is "stable" because the relationship is 10 years deep overlooks that buyers do not value relationship depth, they value concentration risk. Reduce the concentration before market.

3. Presenting unadjusted EBITDA

Going to market with raw P&L EBITDA rather than QoE-adjusted EBITDA invites buyers to apply their own adjustments downward. The seller-led QoE positions the seller's preferred adjustments as the starting point.

4. No documented succession plan

Buyers underwrite the post-acquisition transition. A founder with no documented succession plan, no second-tier leadership team, and no client transition mechanics receives multiple discounts proportional to the integration risk.

5. Founder cannot articulate the business model

The founder who cannot explain the firm's defensible moat, sector authority, and growth trajectory in 30 minutes cedes pricing power to the buyer. The equity story must be tight, evidence-based, and consistent across all buyer conversations.

6. No quality-of-earnings preparation

Buyers commission their own QoE if the seller has not. The buyer's QoE will surface adjustments the seller cannot rebut without preparation, which compresses final price by 5-15%.

7. Going to market without value driver optimisation

The founder who reaches the desired retirement timing and goes to market immediately leaves 30-40% of value on the table. The 24-36 month preparation window is the highest-leverage exit decision.

8. Hiring broker too late

The investment banker or M&A advisor hired 3 months pre-market cannot complete buyer landscape mapping, equity story development, and process design in time. Engage 12 months pre-market.

7-step playbook to maximise valuation

Score the 7 value drivers honestly

Workshop with partners. Score each driver 1-5 with evidence. Identify the 2-3 highest-leverage gaps. Founder dependency, customer concentration, and recurring revenue are typically the highest-impact gaps for boutiques.

Map the buyer landscape

Identify 15-25 named buyers across strategic acquirers (large search firms acquiring niches), PE platforms (buy-and-build investors), PE add-on candidates (existing platforms in adjacent verticals), and management buyout. Research recent deals for precedent multiples.

Eliminate the founder bottleneck

Hire or promote BD specialist coverage. Document the founder-held client relationships. Build the relationship transition mechanics that demonstrate the firm is a transferable business rather than the founder's personal job.

Reduce customer concentration

If top 5 clients exceed 50% of revenue, accelerate new client acquisition in the dominant niche. Target reducing top client to below 20% of revenue, top 5 clients to below 40%.

Build recurring revenue layer

Add RPO contracts, retained advisory engagements, talent intelligence subscriptions, or sector research products. Target 20-30% recurring revenue mix to unlock the 2-3x multiple premium that recurring revenue commands.

Run seller-led quality-of-earnings

Engage QoE advisor 9-12 months pre-market. Adjust EBITDA to reflect normalised owner compensation, one-time items, related-party transactions. Document working capital normalisation. The seller-led QoE positions the firm at the upper end of the multiple range.

Engage M&A advisor and run controlled process

Engage investment banker 12 months pre-market. Co-develop equity story, buyer landscape, process timeline. Run controlled auction with 8-15 named buyers. Multiple competing offers drive the multiple to the upper end of the range. Compare buyer terms beyond headline multiple (earnouts, seller financing, rollover equity, employment continuity).

Architect Your Firm's Exit Multiple

peppereffect installs the value driver optimisation that compounds boutique executive search firm valuations from 4x to 10x EBITDA over the 24-36 month exit preparation window. We engineer the founder dependency reduction, customer concentration mitigation, recurring revenue infrastructure, operating system documentation, and AI augmentation layer that materially expand exit multiples. The Freedom Machine for global boutique recruitment firms.

Frequently Asked Questions

How are recruitment firms valued?

Recruitment firms are valued primarily on adjusted EBITDA multiples. For owner-operator firms below $5M revenue, Seller's Discretionary Earnings (SDE) is the alternative metric that adds back owner compensation, owner benefits, and one-time items. For firms above $5M revenue with a functional management team, EBITDA is the standard. Typical EBITDA multiples range from 3-5x for contingency search firms, 5-8x for retained executive search boutiques, 6-9x for multi-vertical hybrid firms with practice areas, 6-10x for RPO firms with recurring contract revenue, 8-12x for niche specialist retained search, and 10-15x or more for top-quartile niche firms with recurring advisory revenue. Quality-of-earnings analysis adjusts reported EBITDA to reflect true ongoing earning power.

What is the typical EBITDA multiple for a boutique executive search firm?

Retained executive search boutiques typically trade at 5-8x EBITDA, with niche specialist retained boutiques commanding 8-12x. The boutique that combines niche sector authority, recurring advisory revenue, and low founder dependency reaches the 10-15x upper band. The boutique with founder dependency, customer concentration, and inconsistent EBITDA history trades closer to 4-6x. The 5x spread between low and high multiples on identical EBITDA explains why value driver optimisation is the highest-leverage strategic discipline for exit-bound boutique founders.

What are the 7 value drivers that maximise recruitment firm valuation?

The 7 value drivers are: 1) Revenue concentration with top 5 clients below 40% of revenue; 2) Repeat client share of 60-75% of revenue; 3) Recurring revenue from RPO contracts, retained advisory, or talent intelligence subscriptions; 4) Consultant retention of 82%+ annually with bench depth of 2+ partners ready to step up; 5) Sector authority and defensible niche position with documented thought leadership; 6) Operating system documentation including written operations manual, CRM discipline, and governance cadence; 7) Founder dependency with founder generating less than 40% of mandates personally. Each driver scores 1-5 in the standard M&A advisor evaluation. A firm scoring 5/5 on all seven drivers commands the upper band of the multiple range.

How long does it take to prepare a recruitment firm for maximum exit value?

The optimal preparation window is 24-36 months pre-exit. Phase one (months 1-12) focuses on de-risking through founder dependency reduction, customer concentration mitigation, and operations manual documentation. Phase two (months 13-24) focuses on growth acceleration through AI augmentation, recurring revenue base building, and EBITDA margin expansion. Phase three (months 25-36) focuses on market preparation through M&A advisor engagement, quality-of-earnings analysis, buyer landscape mapping, and management presentation development. Firms that skip the preparation window typically achieve 60-70% of their maximum achievable value.

What is the difference between strategic and PE buyers for recruitment firms?

Strategic acquirers (large search firms like Korn Ferry, Russell Reynolds, Heidrick adding niche specialists) typically pay 8-12x EBITDA for true sector authority because the synergy premium reflects revenue synergies, cross-sell opportunities, and brand expansion. Private equity platform investments pay 6-10x EBITDA when establishing a new platform for buy-and-build growth. PE add-on acquisitions to existing portfolio companies pay 5-8x EBITDA with cost synergy focus. Management buyouts pay 4-7x EBITDA typically with seller financing structures. The optimal exit auction includes 8-15 named buyers across all four categories to maximise competitive tension.

What are the most common pitfalls in recruitment firm valuation?

The 8 most common pitfalls are: 1) Relying on revenue multiples rather than EBITDA multiples; 2) Ignoring customer concentration risk; 3) Presenting unadjusted EBITDA rather than QoE-adjusted EBITDA; 4) No documented succession plan; 5) Founder cannot articulate the business model and equity story; 6) No seller-led quality-of-earnings preparation; 7) Going to market without value driver optimisation; 8) Hiring M&A advisor too late. Each pitfall is preventable with disciplined 24-36 month preparation, value driver scorecard, and engagement of professional M&A advisory team 12 months pre-market.

How do I increase my recruitment firm's valuation before selling?

The 7-step playbook: 1) Score the 7 value drivers honestly with the partner team; 2) Map the buyer landscape with 15-25 named acquirers across strategic, PE platform, PE add-on, and MBO categories; 3) Eliminate the founder bottleneck by hiring or promoting BD specialist coverage; 4) Reduce customer concentration to below 20% top client and 40% top 5 clients; 5) Build recurring revenue layer through RPO contracts, retained advisory, talent intelligence subscriptions targeting 20-30% recurring mix; 6) Run seller-led quality-of-earnings 9-12 months pre-market; 7) Engage M&A advisor 12 months pre-market and run controlled auction process. The compounding effect of disciplined value driver optimisation typically expands exit multiples from 4-6x to 8-12x, doubling or tripling exit proceeds on identical EBITDA. succession planning advisory revenue layer brand discipline that drives multiple premium

Resources

- Equidam EBITDA multiples by industry

- Multiples.vc recruitment and staffing valuation multiples

- ValuAnalytics recruiting and staffing valuations

- FirstPageSage EBITDA multiples by industry

- Hunt Scanlon growth and M&A activity surge 2025

- Hunt Scanlon market shift and founder-led exit valuations

- Hunt Scanlon Top 50 Executive Search Firms

- Bullhorn GRID 2026 Industry Trends Report

- RPO Media: Valuation benchmarks for niche recruiting firms

- ClearlyAcquired: EBITDA versus SDE methodology

- Warren Averett: Quality-of-earnings analysis

- Wall Street Prep: Normalised EBITDA

- Windes: EBITDA normalisation

- Brentwood Growth: Owner involvement and valuation

- SE Advisory: Founder dependency as hidden valuation killer

- Morgan and Westfield: Reducing concentration of risk

- CorpInvest: Factors that turn 3x EBITDA into 5x

- Auxo Capital Advisors: Why strategic buyers pay more

- Lion Business Brokers: PE consolidators buying staffing firms

- Dars Law: Management buyout exit strategy

- Recruiter Insider: How to boost valuation before selling

- Talant Staffing: Maximise staffing firm valuation

- Russell Reynolds acquires Savage Partners

- RGF Staffing CSI Companies acquires MedSys Group

- Rob Go: Non-recurring revenue businesses

- BCG: High performers in cyclical sectors

- Equiteq ESG consulting M&A report 2026

- Staffing Hub: Trends that shaped 2025

- Aventis Advisors: Tech company valuation multiples